Hydroxychloroquine: What goes up… stays up?

In our first report, we chose to write about generic Gleevec (imatinib mesylate) – a relatively new generic drug – to highlight the complexities in our drug supply chain that are preventing cost savings for this critical drug from flowing through to payers and patients. If you had a chance to poke around in our 46brooklyn Medicaid Drug Pricing Heat Map, you have likely seen several examples of name-brand drugs that recently went multiple-source generic (e.g. Abilify, Invega, Pristiq, Relpax, Zetia, Seroquel XR, Strattera, Valcyte) where savings are not being fully passed through in all states.

In this report, we will explore a completely different type of drug. Based on our analysis of the FDA’s databases, hydroxychloroquine (generic Plaquenil) has been out for over 22 years now. In other words, this drug – prescribed to treat malaria and several autoimmune diseases – is no spring chicken. So as you would expect, after years of being on the market, it was cheap. VERY cheap. On average, pharmacies were purchasing this drug for $0.10 per tablet at the start of 2014. On average, Medicaid paid $0.21 per tablet in the first half of 2014, and all was well.

But as is normally the case, we don’t learn much about a system if we observe it while it’s in steady state. We need to stress-test a system to see what happens in times of volatility. Sadly, when it comes to hydroxychloroquine, this system largely failed its stress test.

In late 2014, there was a supply shortage, which drove up the pharmacy acquisition cost of hydroxychloroquine from $0.10 per tablet to $2.39 per tablet in just one year. Supply shortages unfortunately happen from time to time for any number of reasons. The good news with this drug shortage was that the marketplace corrected this problem, bringing the price of hydroxychloroquine all the way back down to $0.39 per tablet in early 2018. However, the price that many state Medicaid managed care programs paid for this drug did not decline in line with the marketplace deflation. In Q1 2018, managed care programs are on average still paying $1.25 per tablet, with one paying as much as $2.54 per tablet.

So there is a problem with this drug’s price. Who cares?

In our opinion, the pricing trends of hydroxychloroquine is a problem, just as the Medicaid pricing of imatinib and other new generics is a problem. And even if you're of the opinion that everything gets sorted out on an aggregate basis, we still believe it's important to highlight disturbing trends in the program, in case these pricing tactics are also being deployed in Medicare and commercial plans, where the impact on an employer or patient could be substantial.

More importantly, we would urge you to think again if you believe that things are getting sorted out in the aggregate. At least be open to revisiting that opinion after you see this next (unbelievable) visualization, created by Our World in Data. Not only are things not sorting themselves out... there is an argument to be made that the U.S. has the least efficient healthcare system in the developed world.

We like to think of this complicated system this way: our healthcare system is an expansive ocean that is arguably highly polluted. This ocean is made up of a near infinite number of droplets of water – each which could be contributing to the overall pollution. Generic Gleevec is a droplet. So is hydroxychloroquine. These are the details, and given the mediocre performance of our overall healthcare system, we can't ignore the details.

So 46brooklyn Research can’t think of a better plan than siphoning out one detailed droplet of water at a time and putting it under a microscope to see what’s wrong with it. When the microscope is not readily available in the public domain, we’ll do our best to build one (i.e. visualizations), and then share it with you so you can start siphoning droplets yourself. The more droplets we analyze, the closer we will come to understanding how to properly correct the devastating trend presented by Our World in Data. At least that is our hope.

With that as context, let’s dig in to the story of hydroxychloroquine and see what we can learn.

A fragile marketplace

Brand-name Plaquenil was first released in 1955 to treat malaria and a variety of autoimmune diseases. The generic version, hydroxychloroquine, hit the market in late-1995. Fast forward to late 2013 and the hydroxychloroquine market appeared on the surface to be quite healthy – at least half a dozen manufacturers had competed the price down to $0.10 per tablet. By all accounts, this was a very cheap, mature generic drug. Great news, especially since this is a very important medication, at least according to the World Health Organization, who included it on their WHO Model List of Essential Medicines.

In hindsight, there were signs that not all was well with the hydroxychloroquine marketplace. While there were more than enough manufacturers to drive healthy competition, market share was extremely skewed towards one manufacturer, Ranbaxy Laboratories (now Sun Pharmaceuticals). We merged manufacturer name (by National Drug Code, “NDC”) into CMS’s State Utilization Data to assess this, at least within Medicaid. In the first quarter of 2014, Ranbaxy had 85% market share of all Medicaid program dispensing of this drug. Not a great situation to be in for Medicaid, especially in light of what happened next.

Starting in 2012, Ranbaxy Laboratories ran into a batch of regulatory issues with the Food and Drug Administration (FDA). Specifically, in early 2014, the FDA shut down Ranbaxy’s ability to distribute many drugs in the United States due to what the FDA dubbed significant violations of current good manufacturing practice (CGMP).

This caused an earthquake in the distribution channel. The Wall Street Journal predicted in January 2014 that the sanctions could cause disruptions with several high-profile generic drugs produced at Ranbaxy facilities, including fenofibrate, valganciclovir, and the pending initial release of generic Nexium (esomeprazole). This notably also included hydroxychloroquine, especially given Ranbaxy’s disproportionate share of the US market.

The Journal was right about the FDA actions possibly causing a disruption. A shortage on hydroxychloroquine ensued. The American Society of Health-System Pharmacists (ASHP) fortunately has a handy drug shortage tracker, and they highlighted the hydroxychloroquine shortage as well.

This change had an obvious and profound impact on patients. The Lupus Foundation of America issued a special bulletin in October 2015, shortly after the price of hydroxychloroquine hit its peak. They stated, “Initially, there were widespread reports of shortages and difficulty accessing the drug, but now the primary issue is the spike in price.”

They went on, “We are concerned that constituents may stop taking the drug or ration the drug without their doctor’s knowledge. This is can be very dangerous.”

While drug price spikes are not necessarily uncommon, what happened to hydroxychloroquine was way outside the norm. In the 2016 GAO generic drug price report, they identified hydroxychloroquine as just one of 15 medications that had increased by more than 1,000% from 2010 to 2015, and this one specifically had increased more than 2,500%. As a necessary drug for many patients, this cheap generic had turned into a budget buster.

Mount Hydroxychloroquine

The beauty of free markets is that given proper conditions, they should eventually repair themselves. With the majority of the hydroxychloroquine supply taken off the U.S. market in 2014, the price ballooned to $2.62 per tablet by mid-2015. Outsized profit potential attracted several new competitors who entered the market, drove up the supply, and whittled the price down to $0.39 per tablet as of CMS’s most recent monthly survey (June 2018 prices). The pricing chart, which you can pull up using our 46brooklyn Drug Pricing Dashboard, is shown in Figure 1. We call it “Mount Hydroxychloroquine.”

Figure 1

Source: CMS NADAC database, FDA product/package tables; 46brooklyn Research

What we pay is not necessarily what it costs

However, as we highlighted in our Gleevec report, what we pay for a drug is not necessarily what it costs. So the next logical question becomes, are our states’ hydroxychloroquine costs coming down with the actual price of the drug? Returning to our mountain metaphor, are Medicaid programs hiking down the other side of the mountain and capturing lower costs? Or are they camping out at the peak, stuck in a snowstorm of higher expense?

The good news is that a lot of state programs are realizing lower hydroxychloroquine costs, and many of those programs are fee for service. This makes sense given that in 2016, CMS published the Covered Outpatient Drugs final rule and pushed states to move to more objective pricing benchmarks like NADAC by April 1, 2017 within their fee-for-service programs. Overall, in Q4 2017, the average fee-for-service program paid $0.62 per tablet for this drug – only a $0.19 markup above NADAC. Note: Incidentally, a typical hydroxychloroquine prescription is for 60 tablets. A $0.19 markup per tablet would be $11.40 per prescription for pharmacies, right in the ballpark of where most pass-through fee-for-service programs set their professional dispensing fee).

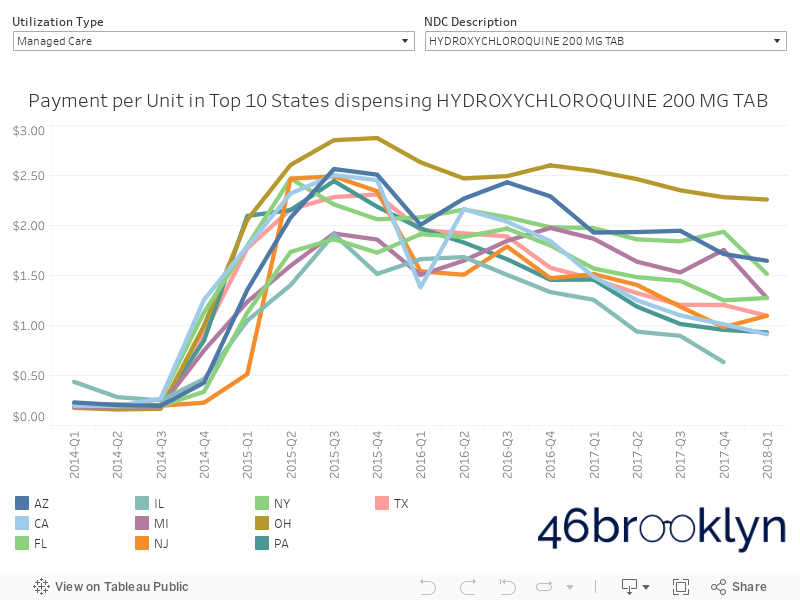

When we look at Medicaid managed care programs, it’s a completely different story. In Figure 2, we developed a “box-and-whisker” plot comparing Q4 2017 hydroxychloroquine costs in fee for service versus managed care. Each dot on the plot is the average amount paid per tablet by a different state. We won’t go into detail on all of the fantastic statistics that this chart provides us, but what’s important to note is that the smaller the “box” (the grey shaded part), the tighter the distribution of the data. So, when we look at fee for service and see a small box, this indicates that states are paying around the same amount for this drug. Shift over to managed care, and states paid anywhere between $0.22 per tablet to $2.58 per tablet in Q4 2017, with a wide range of values in between. This results in a much larger box.

Figure 2

Source: CMS State Utilization Database, CMS NADAC Database, 46brooklyn Research

For those of you that would prefer to see this on a map, Figure 3 shows what this dispersion looks like in managed care, using 46brooklyn’s Drug Pricing Heat Map. Clearly, some state managed care programs are actively hiking down our proverbial mountain towards true hydroxychloroquine cost. On the other hand, a lot of states appear to be – likely without knowing it – still camping out close to the summit.

Figure 3

Source: CMS State Utilization Database, CMS NADAC Database, 46brooklyn Research

Drilling down further, Georgia serves as a good case study for fee for service and managed care program comparison because it has a balanced mix of both programs. We calculate that Georgia’s gross prescription spending split was roughly 60% fee for service and 40% managed care in 2017 – so there is meaningful volume on both sides to compare program reimbursements. Figures 4 and 5 show hydroxychloroquine historical costs for fee for service and managed care in Georgia. Same state, two completely different stories. One very interesting droplet within our healthcare ocean.

Figure 4

Source: CMS State Utilization Database, CMS NADAC Database, 46brooklyn Research

Figure 5

Source: CMS State Utilization Database, CMS NADAC Database, 46brooklyn Research

Georgia isn’t alone. As shown in the following visualization, hydroxychloroquine costs in most states' managed care programs were stuck in a state of suspended animation. Whether these upcharges to the state went to the pharmacies, PBMs, or both really is immaterial to the core issue. The cost burden for this drug simply was – and continues to be – higher than it should be within Medicaid.

Furthermore, in analyzing pricing practices within state Medicaid programs, even though these tactics may not be universally applied in other programs, it is a valid crumb trail to follow to have a hint as to what also may be occurring in Medicare, retirement systems, BWC programs, commercial plans, and perhaps even patients paying out-of-pocket. Make no mistake; if you are a patient suffering from lupus or rheumatoid arthritis, these details matter.

An expensive droplet of water

So how much has our hike up and down Mount Hydroxychloroquine cost? To assess this within Medicaid, we took a look at the pricing change of all generic drugs that, like hydroxychloroquine, were released before 1996. We figured this would give us a good feel for what would have happened to the price of this drug in the alternate universe where there was no FDA shutdown of Ranbaxy's U.S. distribution. Figure 6 shows this comparison. As you would expect, mature generics (like hydroxychloroquine) are cheap, and tend to stay that way. More interesting is that Medicaid appears to be paying almost exactly what these drugs cost – very different from hydroxychloroquine and some of the newer generics we have explored.

Figure 6

Source: CMS State Utilization Database, CMS NADAC Databases, FDA Product/Package Tables, 46brooklyn Research

Armed with this knowledge, we can estimate the cost of the FDA shutdown of Ranbaxy's U.S. distribution. From Q2 2014 through Q1 2018, Medicaid dispensed 125 million tablets of hydroxychloroquine, and paid an extra $1.29 per tablet versus our hypothetical "no disruption" scenario. That's an extra $161 million in under four years – and that doesn't even include the impact to Medicare and commercial plans, or the other drugs impacted by the facility shutdown. Inflated prices in managed care (relative to fee-for-service) was responsible for $28 million of the $161 million.

To be clear, we are in no way implying that the FDA should not have done what it did. But we do believe our analysis does at least bring up some important questions for us to consider:

Should there be greater transparency on drug prices to ensure payers are adequately capturing the savings associated with price deflation?

Should states allow their managed care organizations to enter into contracts that subject them to the risk of overpaying for these sort of drugs?

Should market share among generic manufacturers be monitored to mitigate concentration risk?

Should payers be "insured" in any way from unforeseen generic price spikes?

Should PBMs be responsible for providing this insurance as part of existing services? Or would this type of insurance be better handled by a reinsurer?

Each year, new, expensive drugs are introduced into the market, putting upward pressure on overall drug price inflation. So the older medications need to get cheaper – and then stay cheap – to help mitigate overall drug price inflation. Hopefully we will consider the learnings from the hydroxychloroquine story to keep the cheap drugs cheap and prevent history from repeating itself.