Trump says drug prices are going down. New data shows he’s right and wrong.

As a non-profit, we at 46brooklyn have made it our goal to provide insights into U.S. drug pricing data available in the public domain based upon the figures we’ve gathered over the prior month. Amidst the constant noise about drug prices, these reports act as a reality check of what’s actually happening in the market. This month, we look at what happened in January – which each year is the biggest month for drug price changes. So if you’re interested in drug pricing dynamics, you can expect that 60-70% of all brand-name drug price changes for the entire year will occur withing the first 31 days of the year. Consider today’s report as the tone-setter for the rest of 2026.

Drug Pricing News

The big news of this week was President Donald Trump’s State of the Union address, which was loaded with healthcare bits and pieces and had a dedicated segment on the administration’s efforts to lower prescription drug prices. The transcript from President Trump goes:

“Costs were going to go way up and that's what happened. And now I'm bringing them way down on health care and everything else. I'm also ending the wildly inflated cost of prescription drugs like has never happened before. Other presidents tried to do it, but they never could. They tried. Most didn't try, actually, but they tried.

They said they tried. They couldn't do it. They didn't even come close. They were all talk and no action, but I got it done. Under my just enacted Most Favored Nation agreements, Americans who have for decades paid by far the highest prices of any nation anywhere in the world for prescription drugs will now pay the lowest price anywhere in the world for drugs, anywhere, the lowest price.

So in my first year of the second term, should be my third term, but strange things happen. [Laughter] I took prescription drugs, a very big part of health care from the highest price in the entire world to the lowest. That's a big achievement. The result is price differences of 300, 400, 500, 600 percent and more, all available right now at a new website called trumprx.gov.

And I didn't name that one either, by the way. And here tonight is the very first customer ever to get that big discount, and it is big, Catherine Rayner. For five years, she and her husband have struggled with infertility and they turned to IVF. One drug has been costing Catherine $4,000 to purchase. But a few weeks ago, she logged on to the website and got that same drug that cost costs $4,000, got it for under $500, a reduction of much more actually than $3,500. Catherine, we are all praying for you and you're going to be a great mom.

So now I'm calling on Congress to codify my Most Favored Nation program into law. Now the one thing I'm not sure it matters because it's going to be very hard for somebody that comes along after me to say, let's raise drug prices by 700 or 800 percent. But John and Mike, if you don't mind, codify it anyway.

They may do it. Codify it anyway. Thank you.”

It isn’t the first time President Trump touted his administration’s efforts to lower drug prices, with the first month of 2026 in the books, we can now see what impact the current policies may have had on the bellwether month for price changes directly preceding his speech touting their progress.

Before we get into the data details, a few more news and notes…

January can be a busy month, especially after the holidays and the blur that is the end of year. Like clockwork, January is a month where things begin to pick back up and are often done with more intention. People use January as a reset for their well-being and habits, such as physical activity, eating, or mental health, and many businesses (including the pharmaceutical industry) like to capitalize on this. For example, in January, the much-anticipated first oral version of the hot GLP-1 weight-loss medications made its debut — Novo’s Wegovy tablets — a timeframe that is undoubtedly strategic.

Medication formularies — the curated list of medicines covered under our pharmacy benefit plans — are also “refreshed” in January, a perfect time for manufacturers to increase or maybe decrease the cost (if we are lucky) of certain medications and update their formulary status with government programs and pharmacy benefit managers (i.e. from covered to not covered or prior authorization not required to required, etc.). Towards the end of the year, you may receive a letter in the mail about one or more of your medications and how at the beginning of the new year, there may be some changes — these letters are very important to read and bring to your medical appointments so that you and your provider can potentially establish a plan, whether it is proactively or retroactively. These letters can often be confusing or potentially even overlooked if you just skim through your mail (not that we know what that looks like).

At the pharmacy, once January hits, you may notice a reset of sorts — your yearly deductible has started over. This can come as an unpleasant shock to many, and it might ruin your day or quite honestly your month. Your doable $25 co-pay can suddenly flip to $865.76 in what feels like an instant, which you are somehow expected to pay. Although it may not seem like it, there is may be some light at the end of this dark tunnel.

There have been many steps in the recent years to try to reduce these bloated costs at the pharmacy counter (although the jury is still out on whether or not it is working) from the government stepping in to set drug cost caps for certain medications in Medicare to some popular medications taking price decreases to pharmaceutical companies offering set pricing on certain medications outside of insurance.

On January 27, 2026, CMS announced the selection of drugs for the third cycle of the Medicare Drug Price Negotiation Program. What’s interesting is this round includes the first-ever Medicare Part B drugs, which include certain medications/devices, such as injectables, infusions, or even continuous glucose monitors. There are 15 new drugs (1 drug for renegotiation) that have until February 28, 2026 to decide if they will participate in negotiations.

It’s important to note that while Medicare negotiations for these medications progress, the very first 10 selected drugs by CMS last year just went into effect on January 1, 2026. These medications were initially announced in August 2023 and negotiated prices confirmed in August 2024. It’s still early in the roll-out, so we will see how things have shaken out with the first wave of implementation soon

As mentioned in the President Trump remarks above, another government-backed policy — Most Favored Nation prescription drug pricing — was announced in May 2025 but is now being incorporated into the recently unveiled TrumpRx website, which is largely powered by GoodRx. TrumpRx is a government platform that states that it gives Americans direct access to dramatically lower prices on many common, high-cost brand name prescription products. While it is a short list of medicines, interestingly enough though, if you click on one of the medications, for example the Wegovy pill, the fine print states that the pricing of the 4mg strength of $149 per month is only available until April 15, 2026 and then goes up to $199. This is exactly the same price you would pay if you go directly to the manufacturer’s website, as their fine print states “For self-pay, patients pay $149 for each month of 1.5 mg and 4mg. 4mg offer only available until April 15, 2026, then $199 per month for 4mg.”

So, while it may seem like TrumpRx is being touted as rewriting the script and bringing major savings to Americans, the touted savings are already up for debate, and it has no material difference than what most the manufacturers are offering on their own websites. There are some exceptions where you need to present a TrumpRx coupon at the pharmacy, but before doing so, it is worth checking the manufacturer’s website for your brand-name medication before heading to the pharmacy.

And when it comes to expectations versus reality, we often find that reviewing data is the best way to differentiate between our perceptions and the true circumstances.

The Drug Pricing Cliff Notes

There were 971 changes in brand-name medication list prices (specifically, wholesale acquisition cost, WAC). This includes 951 price increases and 20 price decreases, which means 931 increases in the net (increases minus decreases). The price change percentages ranged from a decrease of -91.70% (Aminosyn-PF Solution for injection) to an increase of 289.40% (Demerol Solution for injection). Typically, we see price changes all over the board — some of which can be just a few hundred dollars, whereas others are a lot more. Depending on the price of a medication and how much utilization the drug is associated with, even a small overall percentage increase could be substantial enough to be millions of dollars in drug pricing swings.

As mentioned, in January, 20 medications took a price decrease. The 20 medications decreasing in price is an upward trend from the beginning of 2025, where we saw only 7 price decreases overall. While WAC price decreases are generally considered a good thing, as we know these decreases can affect drugmaker rebates. Therefore, if the WAC of a brand medication goes down, this also can impact the amount of rebates and discounts that drugmakers offer on that drug (if this is a foreign concept to you, we recommend you learn more about drugmaker rebates and the “gross-to-net bubble” of brand-name medications.

Some of the biggest and/or most interesting movers to take note of for January 2026 were:

Cosentyx Solution for injection (6.3% increase; $1.3 billion PYME)

Stelara Solution for injection (5.0% increase; $1.5 billion PYME)

Invega Sustenna Suspension for injection (2.4% increase; $1.8 billion PYME)

Vraylar oral capsule (5.0% increase; $1.6 billion PYME)

Skyrizi Solution for injection (5.7% increase; $1.5 billion PYME)

Dupixent Solution for injection (5.0% increase; $2.8 billion PYME)

Ozempic Solution for injection (3.0% increase; $3.6 billion PYME)

Trulicity Solution for injection (2.0% increase; $2.0 billion PYME)

Mounjaro Solution for injection (3.0% increase; $1.2 billion PYME)

Eliquis oral tablet (-43.0% decrease; $1.3 billion PYME)

Jardiance oral tablet (-44.4% decrease; $2.4 billion PYME)

Some standout price increases are for medical conditions that include type 2 diabetes (Ozempic, Trulicity, Mounjaro), mental health (Invega Sustenna, Vraylar), and autoimmune disorders (Cosentyx, Dupixent, Stelara, Skyrizi). Some standout price decreases are for type 2 diabetes (Jardiance) and a blood clot preventer (Eliquis). These both also happen to be a part of the CMS 2026 Medicare medications involved in price negotiations. As mentioned above, bear in mind that as you read those numbers, that they are the prices before drugmaker rebates, which as we know are growing significantly over time and are at their largest amounts in the Medicaid and 340B programs.

On the generic side of the coin, year-over-year (YoY) generic oral solid price deflation is at -11.0%, with several interesting generic price trend increases and decreases. But January is almost always a story of brands and this cliff notes is getting a little long, so if you’re interested in more of the details, read on.

What we saw from brand-name medications in January

1. A relatively stable but historically aligned number of list price increases for brand drugs

There were a total of 951 brand-name medications that saw wholesale acquisition cost (WAC) price increases in January and 20 that took decreases, which is featured and contextualized in our Brand Drug List Price Change Box Score, which pulls WAC pricing data from Elsevier. In the net, we had 931 brand price increases which is pretty consistent with past months of January.

Price changes this month ranged from -91.7% to +289.4%.

As a reminder, brand price increases in Medicaid are largely held in check thanks to the Medicaid Drug Rebate Program (MDRP), which includes rebate penalties for drug price increases that occur faster then the rate of inflation. Medicare now has similar cost containment provisions. Commercial employers and cash-paying patients may lack protections from price increases – especially those that occur faster than the rate of inflation.

This is one of a number of reasons that solely analyzing brand list price changes provides an incomplete picture of what’s really happening with brand manufacturer economics, thanks to the growing lot of opaque rebates, discounts, and giveaways that drugmakers shave off those list prices. But alas, until drugmakers, PBMs, insurers, wholesalers, 340B covered entities, and rebate aggregators make more granular data on net prices public, we’ll continue working with what we’ve got.

2. Brand price trends over time

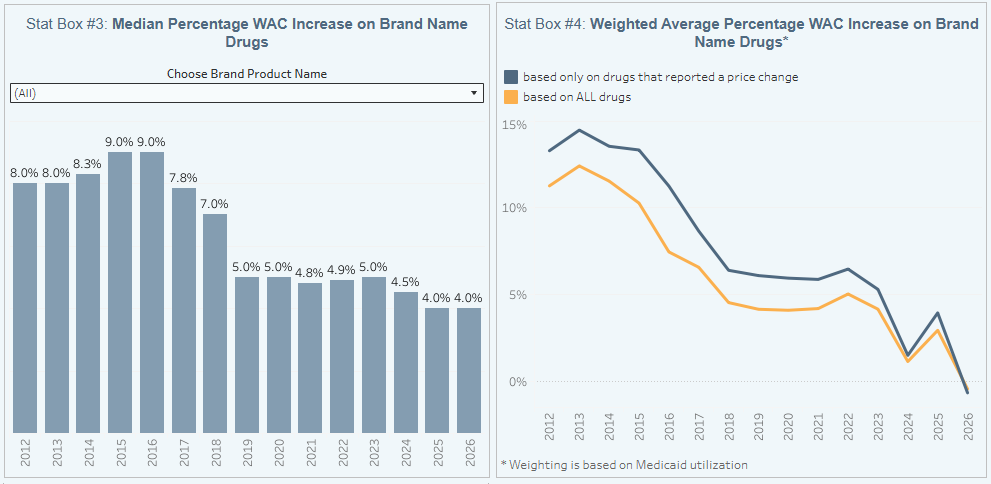

To help contextualize brand name drug list price increase behavior, we find it beneficial to review past trends. In comparison to the data from prior months of January, this year’s net (combined increases and decreases) January price changes seem to line up well with January 2025 (953 net).

The highest recorded number of net price increases occurred in January 2023 with 960 net increases, which means that January 2026 is now the third highest January (at least, as contextualized within our dashboard).

To put it into a more recent perspective (over the last five years) here are the net price increases for each January per year:

January 2025: 953 net brand price increases

January 2024: 873 net brand price increases

January 2023: 960 net brand price increases

January 2022: 807 net brand price increases

January 2021: 797 net brand price increases

Figure 1

Source: Elsevier Gold Standard Drug Database, CMS State Drug Utilization Data, 46brooklyn Research

Of course, we should note that it used to be more common to take price increases twice per year, so in some instances, comparisons to past Januaries miss some of the context.

With this context, one could argue that as far as the actual list prices of medicines go, President Trump may be overstating the market impact he has had, since we are seeing largely business as usual. And if we’re being even more nuanced, you could argue that the number of list price increases this year is among the highest in recent history.

Further examining our brand drug box score visualization, we know that January is increasingly the time of year when most of the brand list price change activity occurs. In an era of increasing scrutiny of drug prices, the growth in the number of price increase events is itself noteworthy, but we need to understand the corresponding degree of price increases to better contextualize these changes (i.e., if 100 drugs take a 10% increase, is that more or less impactful than if 1,000 drugs take a 1% increase?).

When we look at the level of price increase change that is occurring, we see 2026 looking more like 2024 than 2025. First, the median list price increase increase is currently sitting at 4%, which is tied with last year for the lowest level in over a decade. From this perspective, while it isn’t necessarily prices coming down, perhaps President Trump can at least claim this year as a more timid year in terms of the degree of price increases. 4% still clips past overall rates of inflation, but it is a low point nonetheless.

Looking further at Figure 1, we see that those 20 or so brand products that are taking a list price decrease in 2026 are associated with a meaningful degree of utilization (meaning, they are more frequently used by patients). This is because Stat Box #4 tracks price changes overlaid against Medicaid drug utilization data, which gives us a semblance of understanding of the degree with which each drug is actually used in the market. By smashing these datasets together, we get an idea of the proportional market impact each list price change might have on the broader market. This weighted average view is showing a net negative impact of brand list price change behavior based upon the drugs dispensed last year in Medicaid. It comes in at -0.6%. For historical purposes, this only happens if the amount of spending and utilization on those drugs decreasing in price is more than those drugs increasing. We cannot underscore the significance of this enough. What this means is that across 951 brand drug list price increases and just 20 decreases, the impact of those 20 decreases is essentially wiping out the entirety of the impact of the 951 increases. This has never happened in our history of tracking this data. While we would argue that some of public policy decisions that are incentivizing these decreases pre-date the current Trump administration, it would not be inaccurate to state that this administration is in charge during a largely unprecedented drop in the weighted average of brand-name drug list prices.

And given that two of the drugs decreasing in price are some of the most commonly used brands (Eliquis being the top brand by spending in Medicare for years), it makes sense that the data is showing us potentially moving into the Net Pricing Drug Channel (NPDC) that Drug Channels has been telling us is coming.

3. Brand drug list price changes worth taking note of in January

We identify drugs worth taking note of in a couple different ways. Primarily, we look for medications with a lot of prior Medicaid expenditures (not that Medicaid is the end-all-be-all, but it is the only program that regularly publishes past utilization with some decent granularity). We next look for drugs with large pricing changes (+/- 10%). And finally, we look for drugs that are interesting for us either because we’ve previously written on them or because we find them of unique clinical value. And given the number of price changes for brand name drugs in January, well we have a lot to potentially talk about.

OZEMPIC solution for injection (semaglutide) is a glucagon-like peptide 1 (GLP-1) receptor agonist indicated:

as an adjunct to diet and exercise to improve glycemic control in adults with type 2 diabetes mellitus.

to reduce the risk of major adverse cardiovascular events in adults with type 2 diabetes mellitus and established cardiovascular disease.

to reduce the risk of sustained eGFR decline, end-stage kidney disease and cardiovascular death in adults with type 2 diabetes mellitus and chronic kidney disease.

Ozempic took an increase in WAC of 3.0%, impacting $3.6 billion in gross prior year Medicaid expenditures (PYME).

On February 4, 2026, FDA announced its concern about counterfeit Ozempic in the United States. The FDA’s Drug Safety information announcement states that these products may be sold online or there may be versions of the medication that are being sold falsely for research or not for human use. On February 9, 2026, the manufacturer, Novo Nordisk, also took legal action against the popular telehealth platform, Hims & Hers, stating that they have been unlawfully producing unapproved knock-off versions of both Ozempic and Wegovy. Along with all this controversy, the cost of Novo’s shares have recently dropped, causing concern for the company with the potential for sales and profit growth on the decline.

Trulicity solution for injection (dulaglutide) is a glucagon-like peptide-1 (GLP-1) receptor agonist indicated:

As an adjunct to diet and exercise to improve glycemic control in adults and pediatric patients 10 years of age and older with type 2 diabetes mellitus.

To reduce the risk of major adverse cardiovascular events in adults with type 2 diabetes mellitus who have established cardiovascular disease or multiple cardiovascular risk factors.

Trulicity saw an increase in WAC of 2.0%, which impacts $2 billion in gross prior year Medicaid expenditures (PYME).

Like many of the medications spotlighted this month, Trulicity was also selected by CMS as a potential medication to implement starting in 2028 into the Medicare Drug Price Negotiation Program. Otherwise, this GLP-1 from Lilly has not been in the news as much as some of the others.

MOUNJARO solution for injection (tirzepatide) is a glucose-dependent insulinotropic polypeptide (GIP) receptor and glucagon-like peptide-1 (GLP-1) receptor agonist indicated as an adjunct to diet and exercise to improve glycemic control in adults and pediatric patients 10 years of age and older with type 2 diabetes mellitus.

Mounjaro experienced an increase in WAC of 3.0%, impacting $2.5 billion in gross prior year Medicaid expenditures (PYME).

Mounjaro recently had an indication change to reflect that it can now be used in patients 10 years of age and older for the treatment of type 2 diabetes, whereas prior to this, it was only indicated in adults who were 18 years of age or older.

Cosentyx Solution for injection (secukinumab) is a human interleukin-17A antagonist indicated for the treatment of:

moderate to severe plaque psoriasis (PsO) in patients 6 years and older who are candidates for systemic therapy or phototherapy.

active psoriatic arthritis (PsA) in patients 2 years of age and older.

adults with active ankylosing spondylitis (AS).

adults with active non-radiographic axial spondyloarthritis (nr-axSpA) with objective signs of inflammation.

active enthesitis-related arthritis (ERA) in pediatric patients 4 years of age and older.

adults with moderate to severe hidradenitis suppurativa (HS).

Cosentyx had an increase in WAC of 6.3%, impacting $1.3 billion in gross prior year Medicaid expenditures (PYME).

Similar to other pharmaceutical companies that are trying to cut out the “middleman,” Novartis is now offering a direct-to-patient platform (DTP) for Cosentyx. Select units of Cosentyx are available at a 55% discount off list price, which started on November 1, 2025. These DTP (sometimes referred to as direct-to-consumer, or DTC) models offer price transparency while expanding patient reach, including to those without insurance access, while allowing pharmaceutical companies control over pricing, medication distribution, and engagement.

Stelara Solution for injection (ustekinumab) is a human interleukin-12 and -23 antagonist indicated for the treatment of:

Adult patients with:

moderate to severe plaque psoriasis (PsO) who are candidates for phototherapy or systemic therapy.

active psoriatic arthritis (PsA).

moderately to severely active Crohn’s disease (CD).

moderately to severely active ulcerative colitis.

Pediatric patients 6 years and older with:

moderate to severe plaque psoriasis (PsO), who are candidates for phototherapy or systemic therapy.

active psoriatic arthritis (PsA).

Stelara experienced an increase in WAC by 5.0%, impacting $1.5 billion in gross prior year Medicaid expenditures (PYME).

As of January 1, 2026, this medication is one of the first 10 drugs launched by CMS with a negotiated price for Medicare patients. The agreed-to negotiated price for a 30-day supply for 2026 is listed at $4,695.00 versus $13,836.00, which is what it was listed for in 2023. Comparatively, this new price offers a 66% discount.

Skyrizi Solution for injection (risankizumab-rzaa) is an interleukin-23 antagonist indicated for the treatment of:

moderate-to-severe plaque psoriasis in adults who are candidates for systemic therapy or phototherapy.

active psoriatic arthritis in adults.

moderately to severely active Crohn's disease in adults.

moderately to severely active ulcerative colitis in adults.

Notably, Skyrizi had a 5.7% increase in WAC, impacting a $1.5 billion increase in gross prior year Medicaid expenditures (PYME).

DUPIXENT solution for injection (dupilumab) is an interleukin-4 receptor alpha antagonist indicated:

For the treatment of adult and pediatric patients aged 6 months and older with moderate-to-severe atopic dermatitis whose disease is not adequately controlled with topical prescription therapies or when those therapies are not advisable. DUPIXENT can be used with or without topical corticosteroids

As an add-on maintenance treatment of adult and pediatric patients aged 6 years and older with moderate-to-severe asthma characterized by an eosinophilic phenotype or with oral corticosteroid dependent asthma.

As an add-on maintenance treatment in adult and pediatric patients aged 12 years and older with inadequately controlled chronic rhinosinusitis with nasal polyps (CRSwNP).

For the treatment of adult and pediatric patients aged 1 year and older, weighing at least 15kg, with eosinophilic esophagitis (EoE)

For the treatment of adult patients with prurigo nodularis (PR).

As an add-on maintenance treatment of adult patients with inadequately controlled chronic obstructive pulmonary disease (COPD) and an eosinophilic phenotype.

For the treatment of adult and pediatric patients aged 12 years and older with chronic spontaneous urticaria (CSU) who remain symptomatic despite H1 antihistamine treatment.

For the treatment of adult patients with bullous pemphigoid (BP).

Dupixent took a 5.0% increase in WAC, impacting $2.8 billion in gross prior year Medicaid expenditures (PYME).

Although DUPIXENT already has 8 indications Sanofi/Regeneron is looking to add more especially those diseases that are driven by inflammation such as ulcerative colitis and allergic fungal rhinosinusitis (AFRS). The AFRS indication is set to have a target action date or decision by the FDA of later this month on February 28, 2026.

INVEGA SUSTENNA Suspension for injection (paliperidone palmitate) is an atypical antipsychotic indicated for:

Treatment of schizophrenia in adults.

Treatment of schizoaffective disorder in adults as monotherapy and as an adjunct to mood stabilizers or antidepressants.

Invega Sustenna took a 2.4% increase in WAC, impacting $1.8 billion in gross prior year Medicaid expenditures (PYME).

Vraylar oral capsule (cariprazine) is an atypical antipsychotic indicated for:

Treatment of schizophrenia in adults and pediatric patients 13 years of age and older

Acute treatment of manic or mixed episodes associated with bipolar I disorder in adults and pediatric patients 10 years of age and older

Treatment of depressive episodes associated with bipolar I disorder (bipolar depression) in adults

Adjunctive therapy to antidepressants for the treatment of major depressive disorder (MDD) in adults

This medication took a 5.0% increase in WAC, impacting $1.6 billion in gross prior year Medicaid expenditures (PYME).

This medication recently received a new indication and is now approved in pediatric patients for the treatment of short-term manic or mixed episodes of bipolar I disorder in children ages 10 years and older, and treatment of schizophrenia in children ages 13 years and older. Previously, Vraylar was only approved for use in adults, as most patients are not diagnosed with bipolar disorder or schizophrenia until around 15 to 25 years of age.

Now if you notice some drugs missing from our summary, including some of those big decreases, before you complain, be sure you refer to what we put out at the start of the year (we don’t see the point in rehashing what we already wrote).

What we saw from generic medications in January

4. A relatively favorable, unweighted price change picture

Each month, we look at how many generic drugs went up and down in the latest month’s survey of retail pharmacy acquisition costs (based on National Average Drug Acquisition Cost, NADAC), and compare that to the prior month (Figure 2).

Basically, the quick way to read Figure 2 is to look for orange bars that are taller than blue bars to the left of the blue line, and exactly the opposite to the right of the line. That would indicate a good month – more generic drugs going down in price compared to the prior month, and less drug prices going up.

Figure 2

Source: Data.Medicaid.gov, 46brooklyn Research

In looking at the above, for every generic drug that increased in price this past month, 1.13 decreased in price – a slightly favorable view of generic drug price decreases. But as usual, take this unweighted price change analysis with a grain of salt. To really make heads or tails of all of these pricing changes, let’s weight these changes.

5. Weighted Medicaid generic drug costs come in at $37 million in deflation

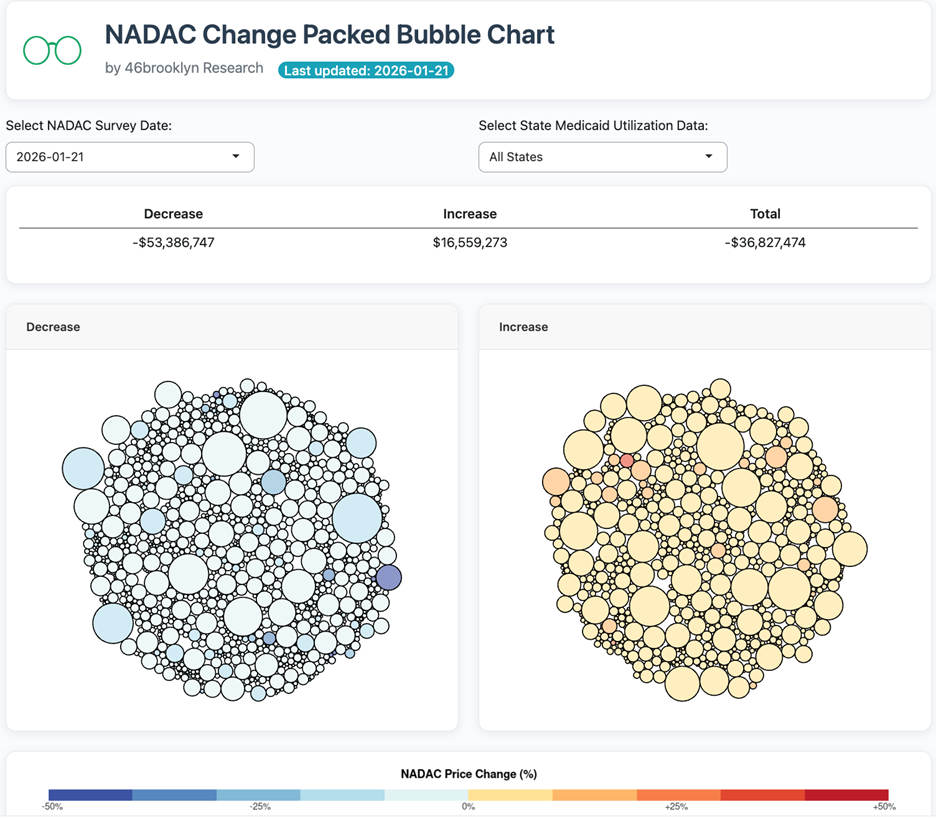

The purpose of our NADAC Change Packed Bubble Chart (Figure 3) is to apply utilization (drug mix) to each month’s NADAC price changes to better assess the impact. We use Medicaid’s 2020 drug mix from CMS to arrive at an estimate of the total dollar impact of the latest NADAC pricing update. This helps quantify what should be the real effect of those price changes from a payer’s perspective (in our case Medicaid; individual results will vary).

The blue bubbles on the left of the Bubble Chart viz (screenshot below in Figure 3) are the generic drugs that experienced a price decline (i.e. got cheaper) in the latest survey, while the yellow/orange/red bubbles on the right are those drugs that experienced a price increase. The size of each bubble represents the dollar impact of the drug on state Medicaid programs, based on utilization of the drugs in the most recent trailing 12-month period (i.e. bigger bubbles represent more spending). Stated differently, we simply multiply the latest survey price changes by aggregate drug utilization in Medicaid over the past full year, add up all the bubbles, and get the total inflation/deflation impact of the survey changes.

Note: You’re not crazy. We changed up the management of this dashboard from Tableau and made some tool enhancements, so it looks a little different than in past updates.

Figure 3

Source: Data.Medicaid.gov, 46brooklyn Research

Overall, in January, there was $16.6 million worth of inflationary drugs, with a offset of $53.4 million of deflationary generic drugs, netting out to approximately $36.8 million of generic drug cost deflation for Medicaid.

These numbers are sort of similar to what we saw in December, where there was around $23 million in inflationary costs with $50 million in deflationary costs, netting out to approximately $27 million.

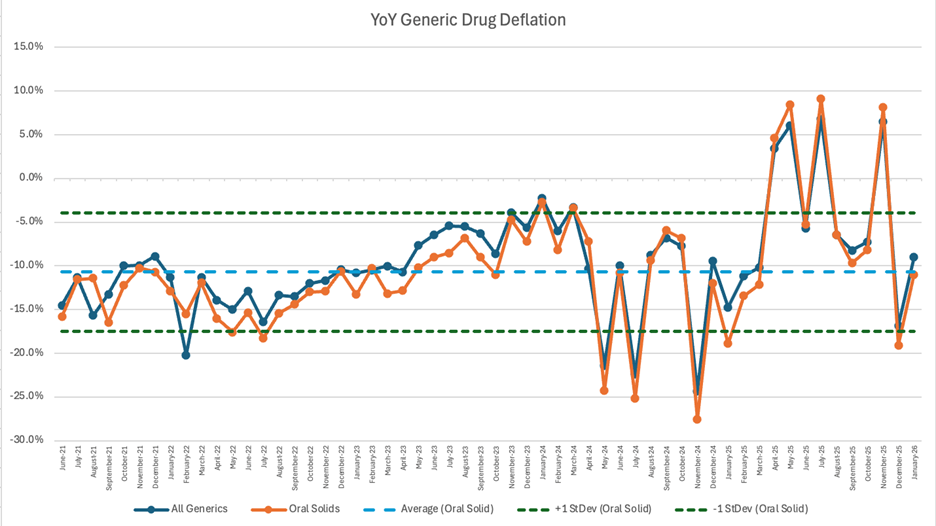

6. Year-over-year generic oral solid deflation at 11%

Ever since June 2020, we have been tracking year-over-year generic deflation for all generic drugs that have a NADAC price. We once again weight all price changes using Medicaid’s drug utilization data. This month, deflation on oral solid generics and all generics was at 11% and 9%, respectively (Figure 4). If you are a purchaser of generic drugs, an increase in this metric is ideal as it means costs are declining. This is right in line with the NADAC packed bubble chart, which also showed the cost of generic drugs decreasing. Businesses generally enjoy it when their input costs go down.

Figure 4

Source: Data.Medicaid.gov, 46brooklyn Research

7. Top/notable generic drug decreases this month

For January, the drug price decreases total $53 million in deflation. After reviewing the various sizes and colors that compromise this month-over-month decrease there are some notable decreases.

The largest outliers in the packed bubble chart this month include ivabradine 5 mg and 7.5 mg, which decreased in price respectively by -31.5% and -17.3%, cyclobenzaprine ER 30 mg, which decreased in price approximately 69%, Tiadylt ER 180 mg, 300 mg, 240 mg, 120 mg, which decreased by approximately 35%, 34%, 32%, and 32% respectively, and phenobarbital 32.4 mg which decreased by 24%.

Ivabradine is an oral tablet used to treat heart failure with reduced ejection fraction. Both oral tablet strengths of 5 mg and 7.5 mg took a decrease in price in January. In March 2025, there was an analysis of the SHIFT clinical trial that showed adding ivabradine to the standard treatment for heart failure significantly improved clinical outcomes. With brand-name medications, it’s not uncommon for good clinical news to be associated with a price increase, but because this drug is a generic, we may see costs actually go down as more people potentially start using it.

Phenobarbital is an oral tablet typically used to treat seizures, and the 32.4 mg tablet decreased by -24%. There have been recent reports from countries including England and Australia where various tablet strengths of phenobarbital are currently in shortage, so it may be a little strange to see it decreasing here.

Cyclobenazprine ER is an oral capsule used to treat muscle spasms. This medication took the biggest price decrease by -69%. Interestingly enough in August 2025, a lower dosage (2.8 mg to be exact) of cyclobenzaprine (brand name Tonmya) was announced as the first new FDA-approved therapy for fibromyalgia in over 15 years. The same pharmaceutical company also plans to try to receive FDA approval using cyclobenzaprine for major depressive disorder with a sublingual dose of 5.6 mg.

Tiadylt ER is an oral capsule used for angina and hypertension and saw price decreases that ranged from 32% to 35% depending upon whether it was the 120 mg, 180mg, 240 mg, or 300 mg strength being viewed.

8. Top/notable generic drug increases

On the increase side of things, notable this month is that only two of the generic drug increases were darker in color in our tool, which means percent changes were on the lower end of the scale — with a couple exceptions. For example, we usually start this section off by noting the most impactful increases of 50% or above, but there aren’t any with that high of a percentage of change.

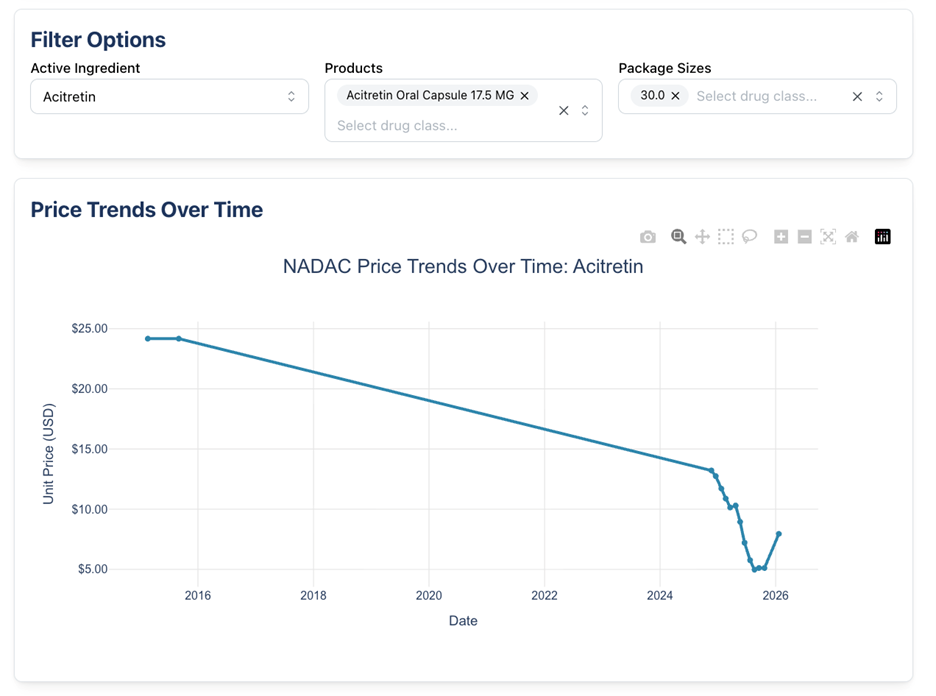

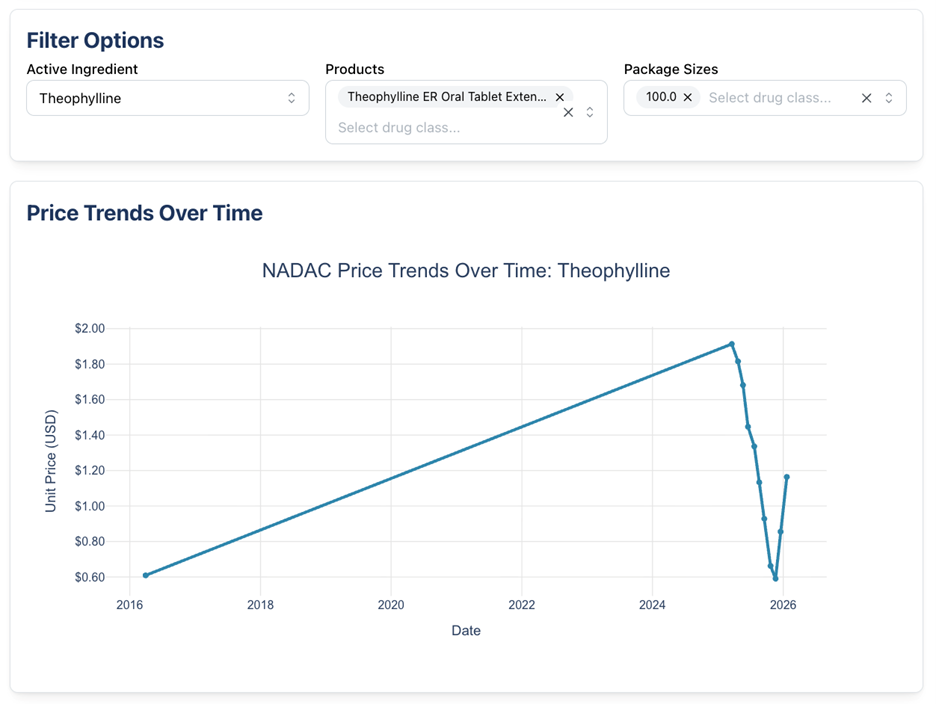

The two generic medications with increases include acitretin 17.5 mg capsule (56% increase) and theophylline ER 450 mg tablet (36% increase).

Acitretin 17.5 mg capsule is an oral medication used to treat severe psoriasis in adults and is the only systemic retinoid for this indication. We’ve reported about this medication, although it was a different strength, back in October 2024. In 2024, the 25 mg capsule also increased in price by 50.9%.

Theophylline ER 450 mg tablet is indicated for the treatment of reversible airflow obstruction in breathing diseases such as asthma, emphysema, and chronic bronchitis. Theophylline is currently on shortage and according to one of the pharmaceutical manufacturers, Glenmark, it is due to manufacturing issues. Both Glemark and Rhodes cannot estimate a release date, but Endo states their product should return in late February potentially.

Below we show what the NADAC trends for these drugs look like:

So, are drug prices going up or down? You be the judge. Keep an eye on our dashboards for month-by-month updates. We will see you soon with more fun and depressing drug channel learnings.

Shout-outs to the following publications for featuring our data and insights over the last few weeks:

Why are Americans paying more for drugs than anyone else in the world?

WJAG-AM Norfolk, 2/17/26

Feds target PBMs’ hidden fees to benefit consultants

Modern Healthcare, 2/12/26

Money from sick people: How PBMs use AWP, spread, and rebates to inflate drug costs

The Benefits Whisperer, 2/10/26

All about pharmacy benefit managers (PBMs)

Las Vegas Public Affairs Show, 2/7/26

White House debuts drug-buying site TrumpRx, with roughly 40 medications

Wall Street Journal, 2/5/26

White House launches TrumpRx discounted drug site

CBS News, 2/5/26

Drug pricing update

Virginia Focus, 2/5/26

Antonio Ciaccia answers the question, "What's a 'base hit' for the pharmacy profession in 2026?"

Pharmacist’s Voice Podcast, 2/5/26

FTC settles lawsuit with Express Scripts over charges it manipulated insulin prices, impeded access

STAT News, 2/4/26

Why cheaper drugs are still out of reach

Washington Post, 1/29/26

This year drugmakers cut prices for several widely used drugs

Wall Street Journal, 1/29/26

Drug pricing discussion with Antonio Ciaccia

Driving it Home with Patti Vasquez, 1/29/26

The hidden economics of drug pricing

Frontier Institute, 1/27/26

Trump says Europe does one thing right: drug prices. ‘A pill that costs $10 in London costs $130 in New York or Los Angeles’

Fortune, 1/21/26

Pharma companies raise list prices, including 16 that had agreements to lower prices with Trump administration: report

PharmaExec, 1/19/26

Drugmakers hike medicine prices in 2026. How much more will you spend?

USA Today, 1/18/26

Trump struck deals with 16 drug companies. But they're still raising prices this year

NPR, 1/16/26

When insurance stops being insurance: Medicare, UnitedHealth, and the generic drug illusion

Raymond Kordonowy Substack, 1/14/26

Surge in Obamacare premiums is symptom of healthcare system in need of reform

Forbes, 1/8/26

U.S. brand-name drug prices fell in 2025 as the net pricing drug channel emerges

Drug Channels, 1/7/26

2026: A tough road ahead in health care

Health Care un-covered, 1/7/26

“Bullshit” — The new way health giants hide billions

Hunterbrook, 1/6/26

Drug companies sign “Most Favored Nation” deals, then raise prices anyway

Drug Discovery & Development, 1/2/26

Upcoming events:

March 5-7: APCI Annual Convention

Antonio Ciaccia presents “The Latest in Drug Pricing Dystopia” with APCI member pharmacies and stockholders

March 16-18: Drug Channels Leadership Forum

Antonio Ciaccia joins Jedi Master Adam Fein for a keynote address and fireside chat at the annual “Wrestlemania for drug channel nerds”

March 25-26: Judi Health Partner Summit

Antonio Ciaccia discusses who pays for drug price hikes with Shawn Gremminger, AJ Loiacono, and Mark Cuban