2026 drug pricing reload: Out with the old, in with the new

Drug prices at the end of 2025, and the start of 2026

As a non-profit, we at 46brooklyn have made it our goal to provide insights into U.S. drug pricing data available in the public domain. We do this by gathering data from often forgotten government websites or from tables of data that do not lend themselves to easy Excel analysis. In a way, it is hard to believe that 2025 is behind us and 2026 is now here, and boy was 2025 a notable year in drug pricing.

At the end of each year, you see on TV, social media, at stores, and everywhere in between the idea of reflecting on the last 12 months. The end of year review or reflections can bring up both positive and/or negative events that have occurred. For example, if you want to know how your music taste has fluctuated throughout the year, you can check out Spotify’s Wrapped; if you want to know how many times you visited Dunkin’ for coffee in 2025, the Rewards Recap email is not afraid to call you out on your coffee and donut habits; if you really crushed your fitness goals this year, Strava’s “Year in Sport” will give a nice summary of your athletic year; and if you’re a Cleveland Browns fan, you get to reflect on what will be next year’s reflection and so on. As fun (or tortuous) as these things are for their users, we’re not aware of anyone that really does something as thrilling as a drug pricing recap and so we figured we would give it a go. And because we cannot do anything exactly like everyone else, we figured we’d sprinkle in a little bit of how 2026 is starting off as well.

If we were to provide a recap of drug pricing activity in 2025, how might we go about doing that? Well, we could start by reviewing the news stories that caught our attention over 2025, then we might analyze some pricing benchmarks to see what that data is telling us about drug pricing in 2025, and we could conclude by taking a peek at what 2026 might have in store for us based upon what happened at the start of the year.

If that sounds like something you’re interested in, then read on.

Noteworthy drug pricing news in 2025

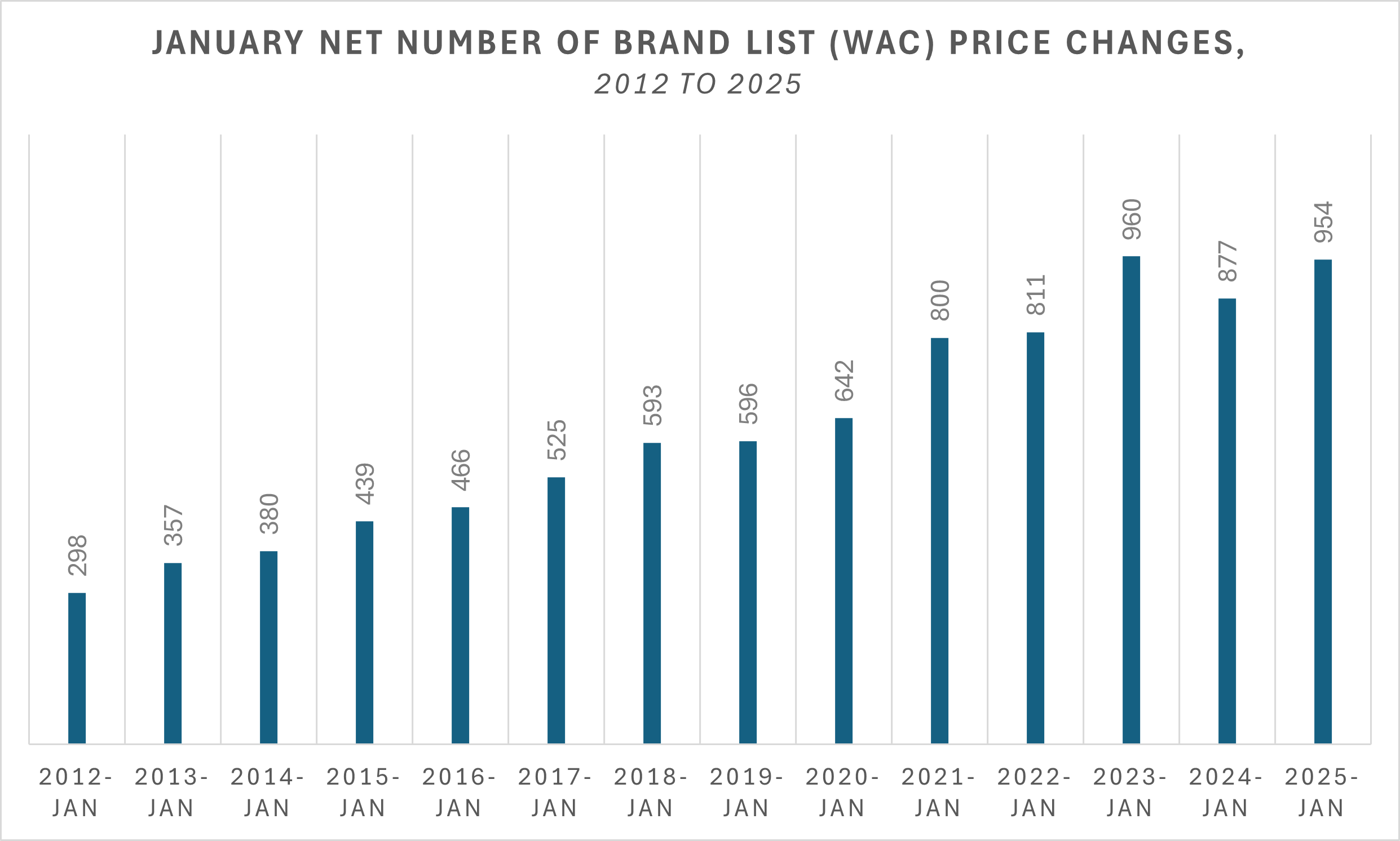

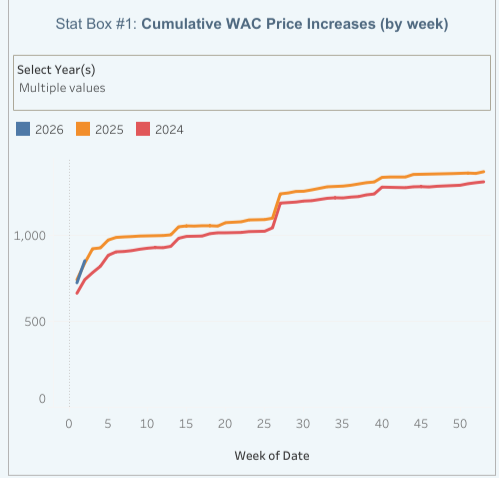

As is typical, 2025 started off with hundreds of brand name drug list price (wholesale acquisition cost, WAC) increases and a small smattering of decreases. This is more or less the same type of news that kicks off each year in drug pricing circles – the only differences being the scope and scale of the changes. To that end, in comparison to other January-ies, 2025 would turn out to be one with a lot of brand drug pricing changes – as in second most of all time per our dashboard when netting out decreases from increases (Figure 1, modified from Stat Box #2 in our Brand Drug List Price Change Box Score):

Figure 1

Source: Elsevier Gold Standard Drug Database, 46brooklyn Research

But monitoring brand drug list price changes were far from the most interesting things to happen at the start of 2025.

In January, Medicare Part D redesign changes went into effect. This included a $2,000 annual out-of-pocket cap for Medicare enrollees (part of a broader shift of more liability on drug spending in Medicare to health plans and drug manufacturers), as well as the ability for Medicare patients to pay as you go with the Medicare Prescription Payment Plan (a policy that allows seniors to smooth their drug costs into monthly installments rather than paying big deductibles all at once at the start of the year). Ultimately, it would seem that seniors wouldn’t really use the payment plan (like less than 1%).

By mid-January CMS had announced the next 15 drugs selected for Medicare price negotiation and the FTC released a second interim staff report focused on the influence that pharmacy benefit managers (PBMs) have over specialty generic drugs (i.e., generic cancer and HIV therapies). The report broadly concluded that otherwise cheap generic drugs (based upon things like pharmacy acquisition costs) were pretty expensive for reasons of PBMs. Coincidentally or not, January 2025 also marked the time that the attorneys for the large PBMs tried to subpoena our communications with the same FTC. Geez, was it something we said?

And at the end of January, in what might have been a blink and you missed it type event given the news flying around at the time, Oklahoma took CVS Caremark to new PBM court over alleged pharmacy underpayments. The Oklahoma complaint identified 200 individual prescriptions for which Caremark paid 15 independent Oklahoma pharmacies less than the drugs' acquisition cost, allegedly violating Oklahoma law.

At the start of second quarter 2025, the FTC would again make headlines announcing a pause in its insulin case against PBMs. The FTC lawsuit had accused the largest PBMs of unfairly limiting access to insulin drugs with lower list prices and steering diabetes patients towards higher priced insulin in order to reap millions of dollars in rebates from pharmaceutical companies.

This announcement was followed closely after by an announcement from the White House – Executive Order 14273, Lowering Drug Prices by Once Again Putting Americans First. This order directed federal agencies to begin to algin US drug prices with the lowest price paid in other developed nations (a concept known as Most Favored Nation [MFN]; see our glossary]. While details were lacking, some additional clarity to this initial executive order was provided in a follow up executive order on May 12. That order, titled Delivering Most-Favored-Nation Prescription Drug Pricing to American Patients directed HHS to set MFN price targets, and enabling direct-to-consumer (DTC) sales at these lower rates, with later actions securing deals on some drugs with companies like Pfizer and AstraZeneca to bring these MFN prices to Medicaid and potentially other programs.

Toward the end of spring, we took note of a nice write up about the state of affairs with State Drug Transparency Laws. As the report outlines, by H1 2025, approximately 23 states had passed some form of drug price transparency laws. In addition, 12 states have created prescription drug affordability boards (PDABs), regulatory bodies that review the affordability and cost of specific prescription drugs in their own respective ways. A lot of these efforts focus on monitoring WAC drug price changes, so hopefully people are continuing to find value in our Brand Box Score.

Quarter 3 2025 drug pricing news began with our much-anticipated gross-to-net bubble sizing refresh from Adam Fein over at Drug Channels Institute – a mandatory annual reminder that the list prices that we track on a week-by-week basis, and that are the scorn of policymakers of all political persuasions, are important but just the top layer of a complex and convoluted drug pricing onion that has more than $350 billion of fluff stuffed underneath.

Shortly after, the Trump administration sent letters to leading drug manufacturers asking/demanding that they match international pricing. As already identified, some of the MFN deals would materialize thereafter. And while the news cycle was probably otherwise slow for drug pricing in Q3 2025 (a lot of eyes were on the upcoming government shutdown), we at 46brooklyn did release our first major piece on PBM private-label products, which gained some attention in the broader policy and drug pricing circles. But perhaps the most interesting things to transpire in the drug pricing space took place in the fourth quarter of 2025.

In October, the Trump Administration launched TrumpRx.gov, a government-operated website whose stated intent is to allow individuals to directly purchase certain drugs — without using insurance – from participating manufacturers at discounted prices. Though details remain sparse (supposedly it’ll start taking orders in January 2026), promises of large discounts were made at the time of the announcement and on the website itself. The announcement of TrumpRx was followed by a November announcements of agreements with manufacturers Eli Lilly & Company and Novo Nordisk, to commit to reducing the prices for certain medications, including Ozempic and Wegovy, when purchased through TrumpRx.gov.

Also in November, CMS announced a new voluntary five-year GENErating cost Reductions fOr U.S. Medicaid (GENEROUS) model, which aims to test an approach, in which manufacturers that participate in the Medicaid Drug Rebate Program (MDRP) provide supplemental rebates to state Medicaid agencies that result in MFN pricing for covered outpatient drugs. That same month, we released our second installment of our PBM private label product series with an in-depth look at Quallent Pharmaceuticals (shout-out to Bloomberg on the excellent coverage).

Finally, organizations like NCPA began advising pharmacies (and the broader public) that WAC price decreases were coming (Fein again had some great commentary on the coming wave). We will revisit this announcement later in this report, but the warning was relevant, as WAC prices play more of a role in pharmacy economics for brand-name medications rather than generics (with the risk being buying inventory at high WAC prices that would be then sold at lower WAC prices — i.e., at a loss).

In short, 2025 was a busy year for drug pricing news and 2026 shows little signs of being any different.

What the drug reference price tea-leaves tell us about 2025 drug prices

As our news review showed, 2025 was a significant year of drug pricing events, but what do prescription drug benchmarks tell us about the state of affairs of drug prices as we look backwards to contextualize what occurred? Well to start, we can look at our Brand Box Score. As a reminder, U.S. pharmaceuticals are generally divided into two categories — brand-name medications and generics. Brand-name medications are those that are patented and granted exclusive marketing rights, whereas generic medications are the cheaper copies made after patents and exclusivity periods have elapsed. Brand-name medications get a lot of the attention in the drug pricing world because they represent 80%+ of prescription drug spending, whereas generics represent about 90% of the prescriptions dispensed but less than 20% of overall drug spending. In other words, while it is far more likely that if you take prescription medications, you are taking a generic medication, the majority of our prescription drug spending wallet goes towards paying for the little bit of brand drug names we do take.

So starting with brands, in 2025, we saw brand-name list price (i.e., WAC) increases across over a thousand products (Figure 2).

Figure 2

Source: Elsevier Gold Standard Drug Database, 46brooklyn Research

This amount of drug list price increase activity in 2025 put it roughly in line with the number of brand list price increases as 2022 and 2023, about 50 more than 2024, and about 300 more than 2021 (the low point over the last five years).

Of course, that number doesn’t tell us a lot about the scale of brand drug price changes. Did a bunch of medications take little price increases or did they take large price increases? Well, ultimately a sense of whether it was “a little” or “a lot” will be a matter of perspective, we we try to present the information within the brand box score in a variety of manners so users can reach their own conclusions.

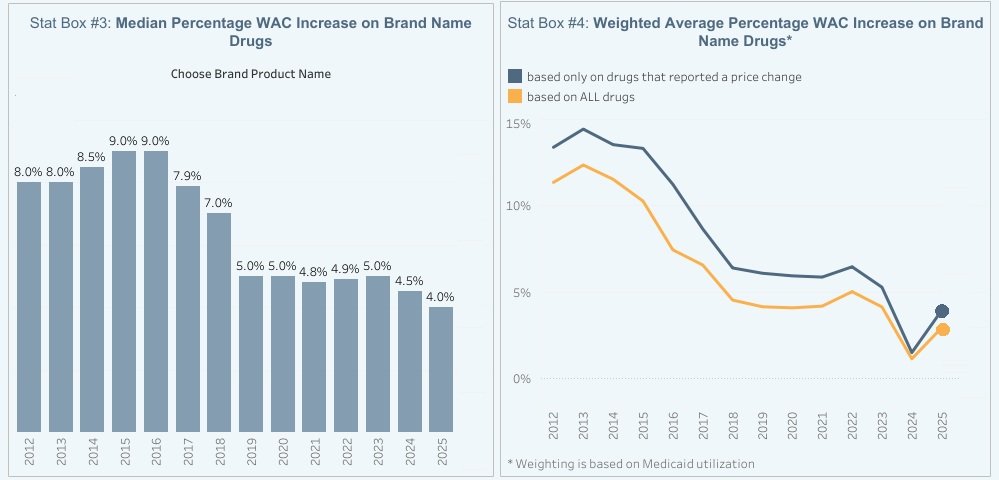

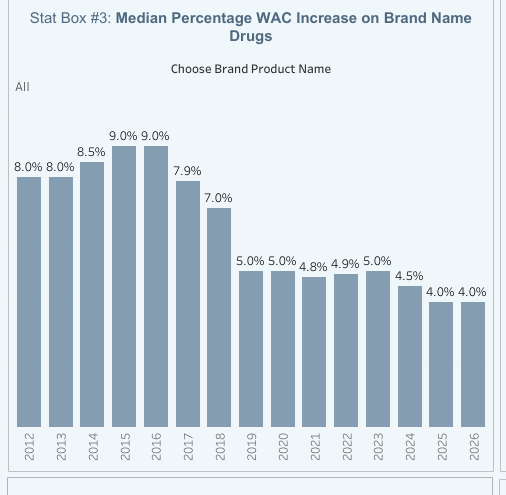

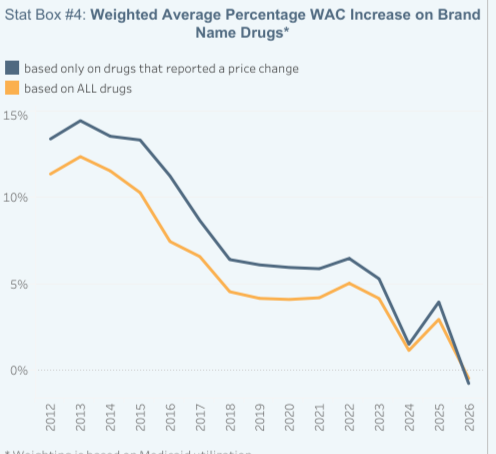

In Stat Box #3, we present the median WAC price change for brand-name drugs over time, and in Stat Box #4, we weight the WAC price change based upon Medicaid utilization of the drug in the prior year (PYME = gross Prior Year Medicaid Expenditures). When we look at 2025, we see that brand-name medications took about a 4% WAC price increase regardless of which of the two Stat Box views we take (Figure 3).

Figure 3

Source: Elsevier Gold Standard Drug Database, CMS State Drug Utilization Data, 46brooklyn Research

Is this a lot or a little? ¯\_(ツ)_/¯

This past year of 2025 is more or less in-line with the trends of the past few years, so maybe neither a little or a lot?

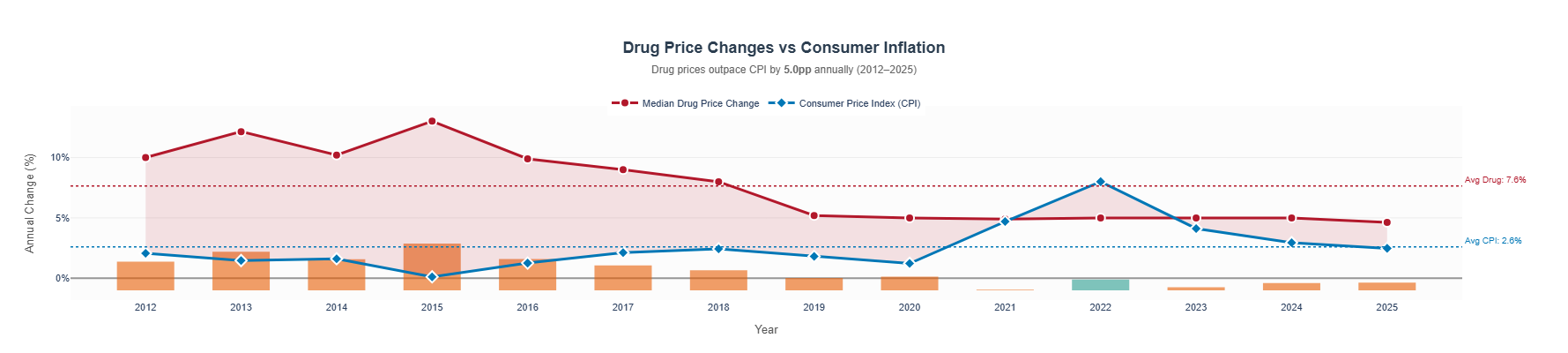

If we use the consumer price index (CPI) as our measuring stick, 2025 brand drug prices would appear to have, on average, increased more than the rate of inflation in the broader U.S. economy. In fact, over the last 14 years, brand drug list prices appear to have exceed average CPI in most years (2022 being the only year where average CPI for the year was above our WAC price increases for the year; Figure 4):

Figure 4

Source: Elsevier Gold Standard Drug Database, U.S. Bureau of Labor Statistics, 46brooklyn Research

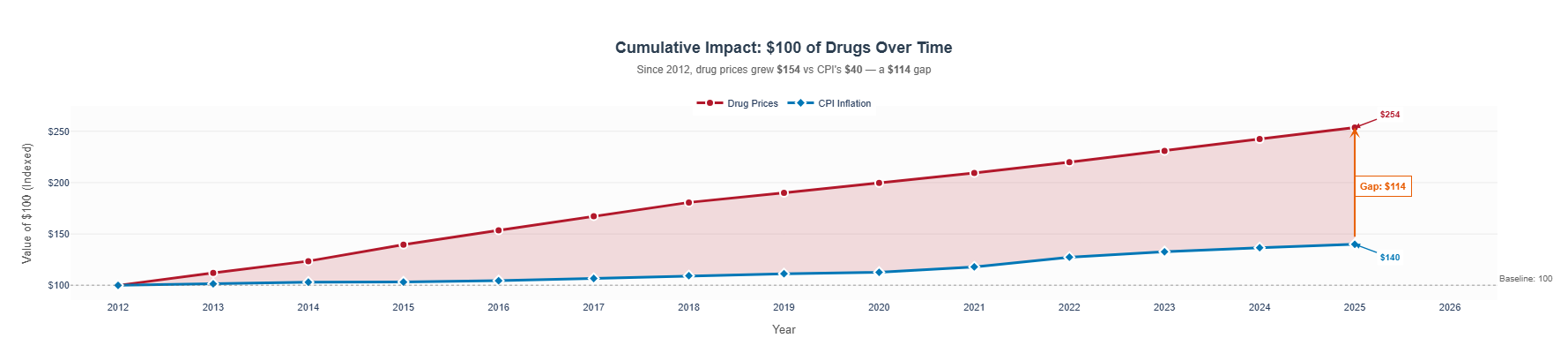

And while a gap of a few percentage points may not seem all that meaningful, if that gap happens consistently over time, the effects compound. In the figure below, we analyze the trend in pricing of a $100 increasing by CPI or by our median brand WAC list price change over time to determine the gap that develops in pricing (Figure 5):

Figure 5

Source: Elsevier Gold Standard Drug Database, U.S. Bureau of Labor Statistics, 46brooklyn Research

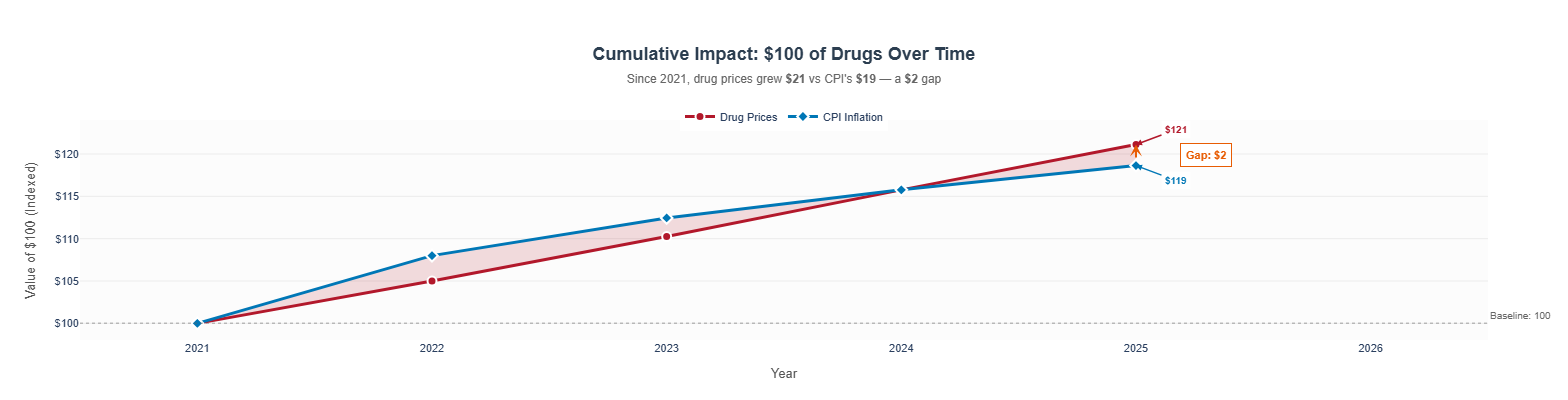

Of course, the world of drug pricing and drug policy was different in 2012 than it is more recently (say post-pandemic). If we change our starting point, the gap between CPI and drug pricing gets a lot more narrow (Figure 6):

Figure 6

Source: Elsevier Gold Standard Drug Database, U.S. Bureau of Labor Statistics, 46brooklyn Research

In other words, when it comes to drug pricing, perspective is often highly relevant to what conclusions we may draw on drug pricing trends.

The aggregate views offered within our brand box score can conceal others of interest. For example, 2024 price change discussions were dominated (at least at the start of the year) buy the insulin brand-name products taking significant list price decreases. These 2024 price decreases were significant for two primary reasons:

The scale of the decreases. The brand-name WAC list prices for the insulins dropped by ~75%.

The number of dollars historically spent on brand-name insulins. Brand-name insulin products were consistently a top 15 therapy in terms of overall drug category expenditures.

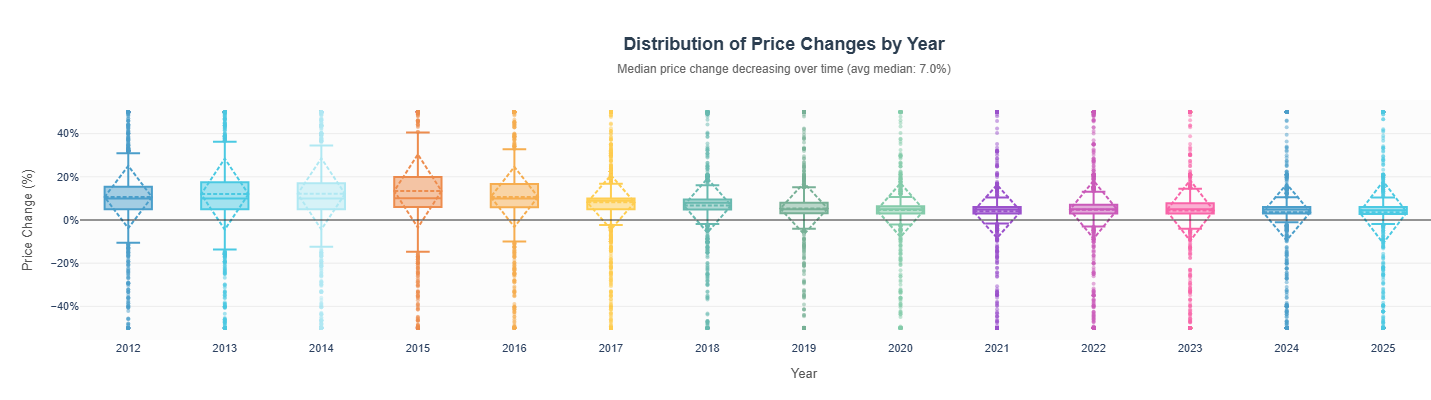

Of course, 2025 had price decreases (including significant list [i.e., 50%] price reductions), but the therapies impacted were not necessarily as commonly used and so they didn’t quite make the same kind of headlines as the 2024 price decreases did. For example, consider what happens if we do more to show the distribution of brand name list price changes year-over-year. In Figure 7 (below) we put the information regarding brand name price changes into a box plot and what we find is that basically every year there are drugs that increase by a lot and little (+/- 50%), but that often times those drugs are not the drugs that really matter (as the weighted average price in any given year is never really near those numbers).

Figure 7

Source: Elsevier Gold Standard Drug Database, 46brooklyn Research

All of this is to say, what is increasing and decreasing is arguably more important than how much the thing is increasing. The 75% price decreases on insulin in 2024 were more impactful than any of the 2024 brand-name drug list price changes (at least in the aggregate; if you don’t take insulin but you take one of the drugs that increased by 10% that year, you may feel differently). For 2025, the top 5 most impactful drugs with price changes based upon our PYME measure were:

Novo Nordisk’s Ozempic saw a 3% WAC list price increase in 2025, impacting approximately $7 billion in annual Medicaid gross expenditures.

Gilead’s Biktarvy saw a 5.9% WAC list price increase in 2025, impacting approximately $6 billion in annual Medicaid gross expenditures.

Sanofi’s Dupixent saw a 5% WAC list price increase in 2025, impacting approximately $4.6 billion in annual Medicaid gross expenditures.

Boehringer Ingelheim’s Jardiance saw a 3% WAC list price increase in 2025, impacting approximately $4 billion in annual Medicaid gross expenditures.

Eli Lilly’s Trulicity saw a 1% WAC list price increase in 2025, impacting approximately $4 billion in annual Medicaid gross expenditures.

Medicaid is a program that expends approximately $100 billion annually. This means that these five drugs represent approximately 1 in 5 gross dollars that Medicaid spends, so monitoring their price moves is meaningful to us all (assuming you’re a taxpayer or Medicaid director). While not appearing within the top 5, we want to give an honorable mention to #20 on the list of PYME impact, Merck’s Januvia saw a 42% decrease in its WAC list price, impacting just over $1 billion in PYME. Spending potentially half a billion less on this drug would be a nice things (and maybe would be true if list prices were the net prices of brand name drugs, but they’re not — especially in Medicaid, where rebates are estimated to be broadly over half the value of the list prices of medicines).

Of course, while brand-name drugs get the majority of the attention (given they’re the majority of the drug spend), they’re not the only way we might think about drug prices changes in 2025. In fact, this section would not feel complete if we didn’t ask our favorite drug pricing benchmark, national average drug acquisition cost (NADAC), what it thought of 2025 price changes.

Recall that NADAC measures the prices pharmacies pay to acquire medications from their wholesalers as measured by their invoice costs (which may or may not be their net price). For most pharmacies, brand drugs are purchased at or near WAC, and so NADAC doesn’t tell us all that much different of a story regarding brand-name drugs from what we saw with WAC (exceptions exist but those are a story for another day, not this recap). However, what NADAC can help us with is filling in the gap of the largest utilized drug category that we haven’t yet talked about — generic drugs. As a benchmark, WAC is not a good measure of what pharmacies pay to acquire drugs. Look at CMS’ own NADAC equivalency metrics to see the delta between a pharmacy’s invoice cost for a generic drug and the WAC benchmark (Figure 8).

Figure 8

Source: Medicaid.gov

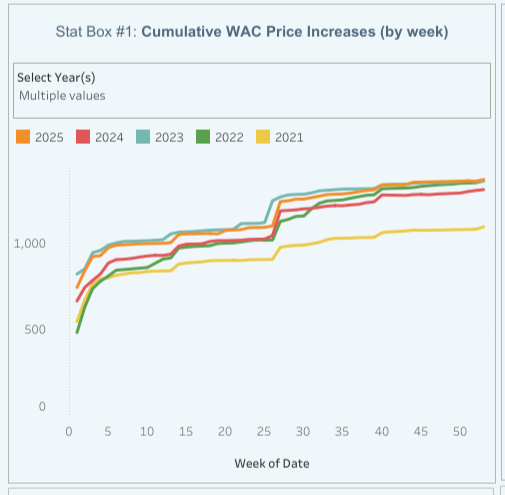

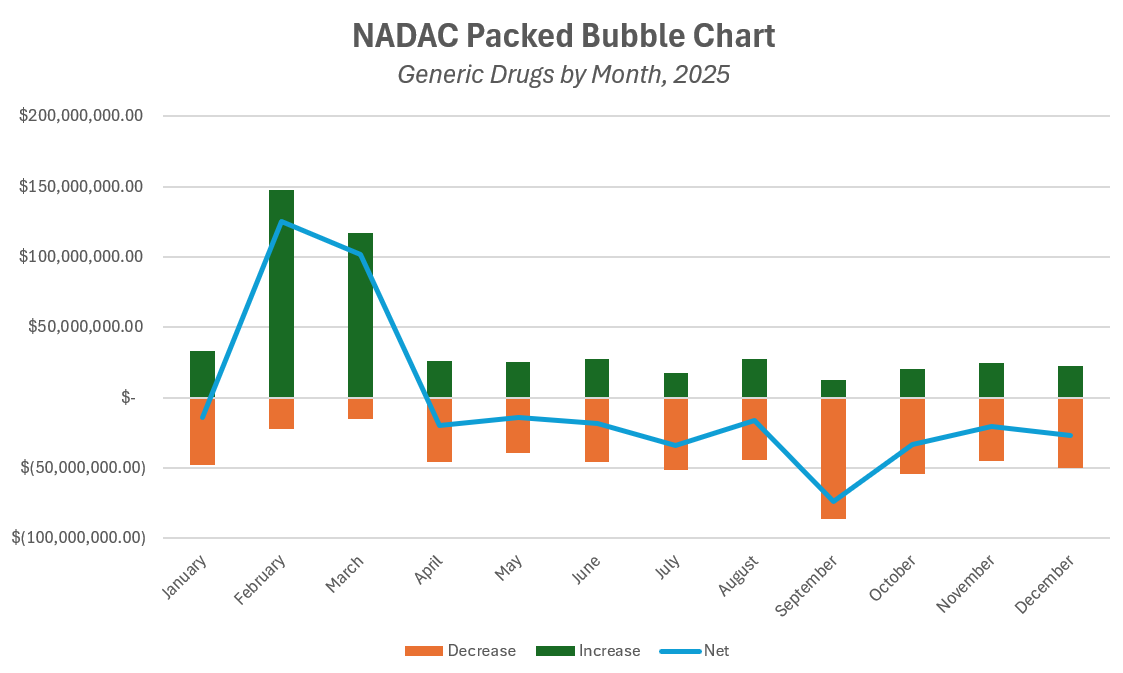

When you buy something for effectively half off or more, that benchmark is generally not a good measuring stick for what that thing costs. Think about it this way, if we have a 1% error in the WAC price of a generic drug, we’re effectively getting an approximate 5% error in the NADAC cost of that thing. Anyway, as it relates to generic drugs, NADAC gives us some interesting signals for what transpired in 2025. To start, we modify our NADAC Change Packed Bubble Chart — the tool we use each month to track aggregate changes in NADAC costs for generic drugs using Medicaid utilization as our measuring stick — to show you what NADAC’s movement looked like throughout 2025 (Figure 9).

Figure 9

Source: Data.Medicaid.gov, 46brooklyn Research

As can be seen above, NADAC skyrocketed for generic drugs at the beginning of 2025 and basically spent the rest of the year working through deflating those costs away. We ultimately ended up in kind of a wash position, where NADAC savings year-over-year where kind of muted for generic drugs. If we look at NADAC price changes from December 2024 to December 2025, we see that on an NDC-basis, the number of generic products seeing an increase in NADAC price (n = 58,372) was not that different from the number showing a decrease (n = 87,888). Of course, what was increasing and decreasing is arguably more important than how much (because as we’ve seen time and again, a little increase for a drug everyone uses is more meaningful than a big increase on a drug no one takes).

So how might we measure which NADAC price changes for generic drugs were most meaningful in 2025? Well, we took a couple of approaches. The top 5 drugs by their NADAC price change delta that resulted in savings (i.e., [(NADAC December 2025 price - NADAC Dec 2024 price) / NADAC Dec 2024 price] were as follows:

ABIRATERONE ACETATE 500 MG TAB saw a 73% decrease in its NADAC price, from $14.05 a tablet down to $3.76 a tablet

BRIMONIDINE-TIMOLOL 0.2%-0.5% saw a 72% decrease in its NADAC price, from $9.41 per mL down to $2.67 per mL

CHLORZOXAZONE 750 MG TABLET saw a 70% decrease in its NADAC price, from $1.90 per tablet to $0.57 per tablet

DILTIAZEM 90 MG TABLET saw a 65% decrease in its NADAC price, from $0.20 per tablet to $0.07 per tablet

NAPROXEN-ESOMEPRAZ DR 375-20 MG saw a 63% decrease in its NADAC price, from $4.80 per pill to $1.78 per pill

On the flip side, the following are the top 5 generic drugs by their NADAC price change delta that got more expensive December 2024 to December 2025:

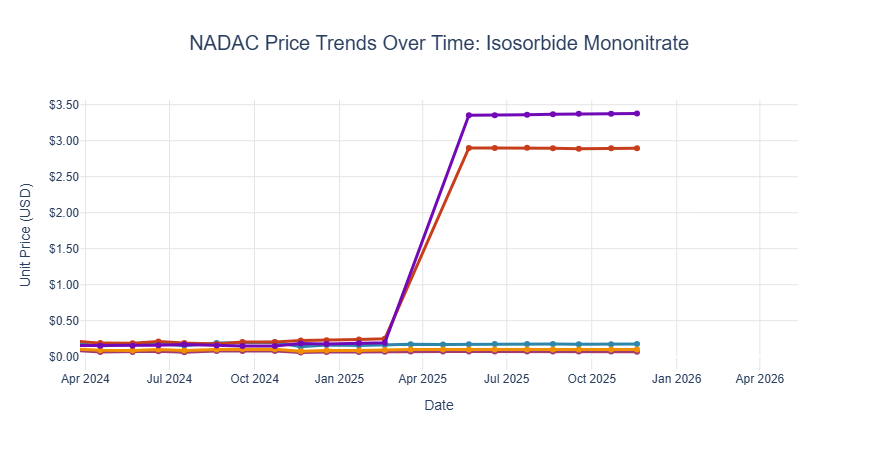

ISOSORBIDE MONONIT 20 MG TAB saw a 1,831% increase in its NADAC price, from $0.18 per pill to $3.39 per pill

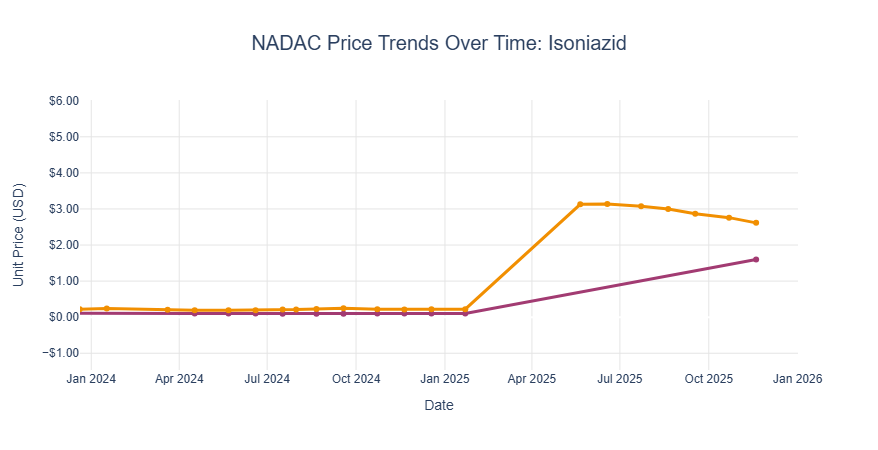

ISONIAZID 100 MG TABLET saw a 1,482% increase in its NADAC price, from $0.10 per pill to $1.61 per pill

ISOSORBIDE MONONIT 10 MG TAB saw a 1,175% increase in its NADAC price, from $0.22 per pill to $2.89 per pill

ISONIAZID 300 MG TABLET saw a 1,125% increase in its NADAC price, from $0.22 per pill to $2.72 per pill

FLURBIPROFEN 100 MG TABLET saw a 878% increase in its NADAC price, from $0.33 per pill to $3.28 per pill

Now while these increases are large on a percentage basis, bear in mind that all of them started from less than $0.50 per pill and have risen to a couple dollars. Furthermore, the reason for these increases is pretty obvious if you have been following drug prices. Isosorbide mononitrate has been in shortage following Teva discontinuing to manufacture the product in December 2024. Isoniazid has been in shortage since March 2025, when two manufacturers stopped making the product. And what’s really great, is even if we didn’t know why these products were increasing in price, NADAC would give us a good signal for when we should go looking for news that may explain the reason for those increased drug prices (Figure 10 & Figure 11).

Figure 10

Source: Data.Medicaid.gov, 46brooklyn Research

Figure 11

Source: Data.Medicaid.gov, 46brooklyn Research

Now, isoniazid in particular is a potentially concerning drug shortage given its role in treating tuberculosis (TB). Treatment protocols have to be modified to help ensure treatment remains effective, which is of particular concern given TB’s resistance to many antibiotic regimens. But if there is a silver lining, it is that not a lot of people in the US need TB treatment. So while the increase is significant, and the cause is known, the overall impact of this price change may not be as significant as it seems. So, in our last attempt to use drug reference prices to tell us what price changes mattered in 2025, the following list is the top 5 of drugs whose NADAC price change was most significant based upon the number of prescriptions dispensed in Medicaid in 2025 (regardless of brand/generic status). Note that in compiling this list, not all of Medicaid’s 2025 State Drug Utilization Data is available, so we’re identifying the drugs simply by the reported number of units at the time of this report, which includes about one full quarter of data.

Ventolin HFA Inhalation Aerosol Solution 108 (90 Base) MCG/ACT saw a 0% change in its NADAC from 2024 to 2025

Fluticasone Propionate Nasal Suspension 50 MCG/ACT saw up to a 10% decrease in its NADAC from 2024 to 2025 (individual package size plays a role on the specific NADAC change)

Ondansetron Oral Tablet Disintegrating 4 MG saw a 1% decrease in its NADAC cost from 2024 to 2025

Vitamin D (Ergocalciferol) Oral Capsule 1.25 MG (50000 UT) saw an 8% increase in its NADAC cost from 2024 to 2025 (note this was a $0.01 increase per pill, as the drug cost in 2024 was $0.10).

Lantus SoloStar Subcutaneous Solution Pen-injector 100 UNIT/ML saw a 0% change in its NADAC from 2024 to 2025 (recall that in 2024 the WAC price decreased by ~75%, which is more or less equal to what happened to its NADAC price)

Hopefully these insights on brand and generic drugs provide some helpful context to the idea of what happened to drug prices in 2025. While the news stories may be the ways most people interact with the drug pricing world, the data suggests that those stories can only scratch the surface of what is going on with the approximately 40,000 unique drug products in the US market — and admittedly, even our data in this report has its limitations (don’t blame us; we want more data). We appreciate, and hopefully you do too, that the answer to whether drug prices went up or down in 2025 can be a matter of perspective. Are we measuring drug prices at the list price level? At the invoice level? In the net? (and if so, whose net price?). The cost to commercial payers? The cost to patients? As we have said many times, until we decide what we want drug pricing to accomplish, we will likely struggle with measuring whether drug pricing policy goals are succeeding.

How are drug prices changing at the start of 2026?

So, while a lot of public focus was given to drug prices in 2025, we suspect that even more attention will be given to drug prices in 2026. And in our drug pricing cycle, we happen to be writing this at the time of the year when all eyes are on the brand-name medication list price changes that kick off each year. And if you’ve been following our work for any length of time, you know this is a busy time for us at 46brooklyn. And the way this calendar fell this year (and given some technical difficulties on the back end that never occur at good times), we were not as on our game this year in getting our dashboard updated at the start of the year. Nevertheless, that didn’t stop the drug pricing stories from flowing already.

First and foremost, 2026 is off to a fast start, with the number of brand name list price changes looking more like 2025 than the lower 2024 (Figure 12).

Figure 12

Source: Elsevier Gold Standard Drug Database, 46brooklyn Research

That’s right, with about half the month already behind us, we’ve seen 872 brand-name products that have already taken WAC list price increases in 2026 alongside 18 decreases (check out recent coverage from NPR and USA Today). Now, as has been the case for years at this point, the median price increase for these products is approximately 4% (Figure 13).

Figure 13

Source: Elsevier Gold Standard Drug Database, 46brooklyn Research

On its surface, it would certainly appear that across 872 increases and 18 decreases, the increases steal the show. However, the real story (at least in our mind) is that much like 2024, that small number of decreases have a system impact that speaks the loudest. And in this context, we use impact based upon the amount of expenditures Medicaid has for the products taking price decreases historically. Because when we do what we typically do, which is try to weight the price changes by the gross Prior Year Medicaid Expenditures (PYME), we see, for the first time, a net negative impact from first of the year drug price changes (Figure 14).

Figure 14

Source: Elsevier Gold Standard Drug Database, CMS State Drug Utilization Data, 46brooklyn Research

That’s right, for the first time ever, when we line up up the price changes next to the historical utilization and expenditures, we get a negative number because the drugs that are decreasing in price are more meaningful collectively than the drugs increasing in price. The drugs and their price decreases are summarized below:

CIMERLI Solution for injection took a WAC list price decrease of 85.30%

FIASP took a WAC list price decrease of 75.00%

TRESIBA took a WAC list price decrease of 72.20%

LINZESS Oral capsule took a WAC list price decrease of 50.30%

SYNJARDY Oral tablet took a WAC list price decrease of 44.40%

SYNJARDY XR Oral tablet, extended release took a WAC list price decrease of 44.40%

TRIJARDY XR Oral tablet, biphasic release took a WAC list price decrease of 44.40%

GLYXAMBI Oral tablet took a WAC list price decrease of 44.40%

JARDIANCE Oral tablet took a WAC list price decrease of 44.40%

ELIQUIS Oral tablet took a WAC list price decrease of 43.00%

FARXIGA Oral tablet took a WAC list price decrease of 37.00%

Now, the list above represents over $5 billion in annual Medicaid gross expenditures (or roughly 1 in 20 gross Medicaid pharmacy dollars). And because the scale of these price decreases is effectively half off, that is a signal that the historic $5 billion in expenditures may be as low as $2.5 billion in the coming year. On the flip side, because the increases are just over 4% on roughly $45 billion in gross Medicaid expenditures, that would only be projected to increase expenditures by just under $2 billion. This means we get a negative impact in Stat Box #4 of our tool. Now, we do not expect Stat Box#4 to stay this way as the year proceeds (unless a whole bunch more brand-name drugs take WAC list price decreases later in the year), but it’s nevertheless noteworthy to be here at this time of January 2026 with such a historic fall of prices for such meaningful medicines.

In reviewing the list above, the list includes several brand medications that were predicted were going to potentially take price decreases (see NCPA’s list for example). A lot of prediction regarding brand drug list price decreases were made due to the drugs being on Medicare’s list of products subject to CMS negotiation that went into effect at the start of 2026 as well. As way of demonstrating, we took the list of Medicare’s first 10 price negotiation drugs and identified what the WAC list price behavior has been (giving green check marks if their price as decreased and red X if their price has increased). What we see is that 6 out of 10 of the drugs have taken WAC price decreases.

Eliquis = ✅, 43% WAC price decrease January 2026

Jardiance = ✅, 44% WAC price decrease January 2026

Xarelto = ❌, 5% WAC price increase January 2025

Januvia = ✅, 42% WAC price decrease January 2025

Farxiga = ✅, 37% WAC price decrease January 2026

Entresto = ❌, 3% WAC price increase January 2026

Enbrel =❌, 5% WAC price increase January 2026

Imbruvica = ✅, 41.5% WAC price decrease December 2025

Stelara = ❌, 5% WAC price increase January 2026

NovoLog/Fiasp = ✅ & ✅ , 75% WAC price decrease January 2024 & January 2026, respectively

Note that Imbruvica took its list price decrease in December 2025 (so it doesn’t show up in our earlier identification of drug price decreases). And while it is true that the WAC list price decreases for many of these drugs do not perfectly align their price with their Maximum Fair Price (MFP), there is undoubtedly some relationship between the drug being part of Medicare drug price negotiations and the drug seeing WAC list price decreases. But simply being part of MFP cannot fully explain why these drugs are taking price decreases, because there are plenty of drugs taking price decreases that are not MFP drugs. For Cimerli, we think the reason that drug price is decreasing is because of a transfer of ownership and new marketing strategy, but why are Linzess and Tresiba on this list? Well, Linzess might be because its on Medicare’s list of price negotiation for 2027 and Tresiba might just be re-aligning its price with the other insulins (since basically all major brand insulins have taken price decreases at this juncture).

In other words, we don’t know really everything regarding these drug price changes for sure except that drugmaker incentives have clearly changed and that we will need to keep watching them to see what happens through the rest of 2026.

So what’s next?

In typical 46brooklyn fashion, we’ve written a novel of drug pricing information (ok, more like a dozen pages worth) when we intended to write a quick update. But we hope you found it all as interesting as we do (and you would not believe what we leave on the cutting room floor trying to shorten these pieces). It seems appropriate to leave a list of the items we’re keeping our eyes on at the start of 2026. And so here is that list of things we’re watching out for (in no particular order):

The first prices of drugs on TrumpRx.gov. We hope that there will be an API or some manner of accessing the prices of the medications in some consolidated way and in keeping with the Great Healthcare Plan’s transparency initiatives (because we would like to get a quick list of all the drugs and to make a bunch of comparisons of TrumpRx prices to NADAC, to WAC, to Cost Plus Drugs, to Medicare, etc).

Whether the list of brand-name drugs taking price decreases continues to grow. NCPA’s list of drugs included some that would take price decreases in February, not January. Is a new normal being established in the age of Medicare price negotiation, a Trump administration seemingly focused on international MFN, and perhaps growing gaps between what manufacturers want drug pricing to accomplish and what PBMs want?

Whether more manufacturers are going to drop off the Medicaid rebate / 340B roster. Effective October 1, 2025, Bausch Health and its subsidiary, Salix Pharmaceuticals, voluntarily ended their Federal Drug Rebate Agreement with the Centers for Medicare and Medicaid Services (CMS). With the 340B rebate pilot paused, will more manufacturers chose this path? We know that Blue Fin Group’s Bill Roth has predicted as much.

Whether Congress will move on any number of prescription drug pricing initiatives. PBM reform has been in the wings for years now, proposals keep growing regarding policies which would help onshore drug manufacturing, and for the first time ever, we might be on the cusp of getting detailed information from health plans regarding their net drug costs due to TiC policies. But until such time as those things move from the theoretical to the realized, we remain on the wings waiting for the next file we can turn into an analysis or new visualization. We hope our wait this year is short, but we’re not necessarily going to be holding our breath.

Shout-outs to the following reporters and outlets providing coverage of the 2026 price changes and our ongoing data tracking:

Pharma companies raise list prices, including 16 that had agreements to lower prices with Trump administration: report

PharmaExec, 1/19/26

Drugmakers hike medicine prices in 2026. How much more will you spend?

USA Today, 1/18/26

Trump struck deals with 16 drug companies. But they're still raising prices this year

NPR, 1/16/26

U.S. brand-name drug prices fell in 2025 as the net pricing drug channel emerges

Drug Channels, 1/7/26

Exclusive: Drugmakers raise US prices on 350 medicines despite pressure from Trump

Reuters, 12/31/25

Lastly, while there is plenty more to catch up on, we’d like to also call out Hunterbrook for their deep-dive on the mysterious world of PBM group purchasing organizations.