No holiday deals on drug prices

The CLIFF NOTES

As a non-profit, we at 46brooklyn have made it our goal to provide insights into U.S. drug pricing data available in the public domain based upon the figures we’ve gathered over the prior month. This month is of course no different, except that we’re getting our analysis out a little later than normal because of the holidays, and the fact that we’ve been cooking up a nice research piece (more on that later).

Fortunately for us, the story this month related to U.S. drug pricing was largely muted. While October saw a numerically high number of price increases (which we predicted two months ago), it was nonetheless a slow month for drug pricing stories. There has still been little movement at the federal level that might shake up the drug pricing world, and so the status quo seems to have held true for October. Said differently, we’re not seeing any holiday deals on the drug pricing front.

While there were a net 45 brand drug list price increases in October, the majority of the price changes were on drugs with less then $10 million per year in gross prior year Medicaid expenditures (PYME). The biggest movers to take note of were Jakafi (2.5% increase; $94.6 million PYME), Idelvion (2.8% increase; $73.5 million PYME), Tyvaso (4.9% increase; $42.2 million PYME), Octagam (4% increase, $33.8 million PYME); Injectafer (3% increase, $33.8 million PYME); Humate-P (2.9% increase, $22.8 million); and Panzyga (1.3% increase, $19.3 million PYME). These products are used to treat a variety of generally rare medical conditions from cancer to hemophilia. Bear in mind that as you read those numbers, that they are the prices before drugmaker rebates, which as we know are growing significantly over time and are at their largest amounts in the Medicaid programs.

On the generic side of the coin, year-over-year (YoY) generic oral solid price deflation compressed a touch to 14% (from 15% a month ago). And while we still see some drugs creeping up in price, none would suggest broad supply chain issues related to drug prices at this point (though we are relying upon lagging indicators).

So as the omicron variant casts an ugly shadow over the national discourse on a number of high-profile policy issues – including drug pricing reform efforts – we again attempt to provide some relevant context to what’s happening in the pharmaceutical trenches. Read on to arm yourselves with the details as they relate to October’s brand and generic drug pricing changes.

Brand Name Medications

1. A small number of list price increases for brand drugs

There were a total of 46 brand-name medications that saw wholesale acquisition cost (WAC) price increases in October and one that took a price decrease, which are all featured and contextualized in our Brand Drug List Price Change Box Score.

Price changes this month ranged from -23% to 68% and impacted $407 million in prior year gross Medicaid expenditures. This is a very similar impact, in terms of Medicaid expenditures, to last month’s figure. As a reminder, brand price increases in Medicaid are largely held in check thanks to the Medicaid Drug Rebate Program (MDRP), which includes rebate penalties for drug price increases that occur faster then the rate of inflation.

This is one of a number of reasons that solely analyzing brand list price changes provides an incomplete picture of what’s really happening with brand manufacturer economics, thanks to the growing lot of opaque rebates, discounts, and giveaways that drugmakers shave off those list prices. But alas, until PBMs, insurers, and rebate aggregators make more granular data on net prices public, we’ll continue working with what we’ve got.

2. Brand price trends over time

To help contextualize brand name drug list price increase behavior, we find it beneficial to review past trends. In comparison to prior years, this past month saw the largest October net (combined increases and decreases) branded price increases since 2017 (when there were 46 net increases). The highest number occurred back in 2014 when there were 185 net October brand list price increases.

Moreover, when further examining our brand drug box score visualization, we continue to see the degree of increases at some of the lowest levels in recent history. Of the drugs that took increases so far this year, the median price increase has been 4.8% – the lowest percentage in over a decade. And when weighting the list price increases using Medicaid drug utilization data, 2021’s brand increases amount to a weighted average of 3.8%, which is a rounding error away from the smallest degree of increases in over a decade as well. All of these are consistent with the last several months we’ve monitored.

3. Brand drug list price changes worth taking note of in October

We identify drugs worth taking note of in a couple different ways. Primarily, we look for medications with a lot of prior Medicaid expenditures. We next look for drugs with large pricing changes (+/- 10%). And finally, we look for drugs that are interesting for us either because we’ve previously written on them or because we find them of unique clinical value. This month, when looking for these drugs in the brand arena, we have a couple of each worth mentioning:

Jakafi (ruxolitinib) is a medication to treat bone cancer or a rare disorder of blood cell production within the bone marrow. This medication took a 2.5% WAC price increase in October, which impacts $94.6 million in gross prior year Medicaid expenditures (PYME).

Idelvion (Factor IX) is a medication to control and prevent bleeding episodes in people with hemophilia B. This medication took a 2.8% WAC price increase in October, which impacts $73.5 million in gross PYME.

Tyvaso (treprostinil) is a medication to treat pulmonary arterial hypertension. This medication took a 4.9% WAC price increase in October, which impacts $42.2 million in gross PYME.

Octagam (immune globulin) is an immune globulin, which can be used to treat immunodeficiency, rare platelet disorder, and a rare condition involving muscle inflammation. This medication took a 4% WAC price increase in October, which impacts $33.8 million in gross PYME.

Injectafer (ferric carboxymaltose) is an injectable iron replacement. This medication took a 3% WAC price increase in October, which impacts $33.8 million in gross PYME.

Humate-P (antihemophilic factor/von Willebrand factor complex) is a factor replacement therapy for people with von Willebrand disease. This medication took a 2.9% WAC price increase in October, which impacts $22.8 million in gross PYME.

Panzyga (immune globulin) is a medication to treat chronic inflammatory demyelinating polyneuropathy, a rare progressive weakness. This medication took a 1.3% WAC price increase in October, which impacts $19.3 million in gross PYME.

Koselugo (selumetinib) is a medication to treat chronic inflammatory demyelinating polyneuropathy, a rare progressive weakness. This medication took a 4% WAC price increase in October, which impacts $12.9 million in gross PYME.

Cinvanti (aprepitant) is a medication used to help control nausea. Aprepitant already exists in other dosage forms, though not injectable like this version. This medication took a 2.2% WAC price increase in October, which impacts $9 million in gross PYME.

Indocin suppositories (indomethacin) is a medication indicated for arthritic conditions. Note that indomethacin already exists in other dosage forms, just not as a suppository. This medication took a 68% WAC price increase in October, which impacts approximately $25,000 in gross PYME. Kudos to Bob Herman at Axios for bird-dogging this one when it hit our dashboard last month.

Carospir (spironolactone suspension) is a medication generally used, in addition to other therapies, to help lower blood pressure. Spironolactone already exists in other dosage forms (i.e., tablets), and was compounded into suspension from tablets for years before this formulation was FDA-approved. This formulation took a 15.5% WAC price increase in October which impacts $3.7 million in gross PYME.

The pricing behavior seen here can be particularly problematic for patients who were getting spironolactone medication cheaper when compounded from their pharmacy before this medication was FDA-approved (note, that compounded formulas for spironolactone suspension have been around since at least the 1980s). However, as with many previously compounded medications, now that this FDA-approved version is on the market, compounding pharmacies may no longer serve some of these spironolactone patients. This is because many states have rules – our home state of Ohio included – preventing the compounding of medications with commercially available formulations. The intent of these rules is to increase patient safety under the auspices that relying upon good manufacturing practices is better then an individual compounding environment at a pharmacy (regardless of whether the drug in question is a high-risk sterile product or not). But when drug companies come and patent copies of a product that has been effectively on the market for years through compounding, and then with the protected patent in hand, increase the price for that product, this can make patient affordability beyond challenging (as seen on Carospir’s website where they predominately display their patient savings card, EasyPay). This can occur not only just due to the higher cost of the drug, but can cause changes in the patient’s plan design. For example, Carospir may now require a prior authorization, but the old compound version may not have due to its low cost. And while we are picking on Carospir a little bit here, since both of the prior drugs in this section – Cinvanti and Indocin – are also re-formulations of existing products, the overall learning here is that the incentives of our current system promote the expenditures of resources (manufacturing power, investment dollars, time, etc.) towards making these ‘me-too’ versions of therapies rather then providing novel clinical therapies. But we digress.

Paxil tablets, Paxil CR tablets, Paxil suspension (paroxetine) are medications used to treat depression. All three formulations have generic versions at this point; however, all three of the brands took 9.9% price increases, impacting a collective $1.2 million in gross PYME.

Phexxi Vaginal Gel (lactic acid, citric acid, potassium bitartrate) is an on-demand birth control. This medication took a 9.9% WAC price increase in October, which impacts approximately $25,000 in gross PYME.

Abilify tablet (aripiprazole) is a medication used to treat schizophrenia. This medication has a generic version at this point; however, this brand took a 23% price decrease impacting $18.6 million in gross PYME.

Generic Medications

4. A mildly unfavorable, unweighted price change picture

Each month, we look at how many generic drugs went up and down in the latest month’s survey of retail pharmacy acquisition costs (based on National Average Drug Acquisition Cost, NADAC), and compare that to the prior month (Figure 1).

Basically, the quick way to read Figure 1 is to look for blue bars that are taller than orange bars to the left of the dotted line, and exactly the opposite to the right of the dotted line. That would indicate a good month – more generic drugs going down in price compared to the prior month, and less drug prices going up.

Figure 1

Source: Data.Medicaid.gov, 46brooklyn Research

Unfortunately, that’s not what happened this month. For every generic drug that increased in price this month, 1.02 decreased in price, considerably lower than the 1.21 ratio last month.

But as usual, take this unweighted price change analysis with a grain of salt. To really make heads or tails of all of these pricing changes, let’s weight these changes.

5. Weighted Medicaid generic deflation comes in at less than $1 million

The purpose of our NADAC Change Packed Bubble Chart (Figure 2) is to apply utilization (drug mix) to each month’s NADAC price changes to better assess the impact. We use Medicaid’s 2020 drug mix from CMS to arrive at an estimate of the total dollar impact of the latest NADAC pricing update. This helps quantify what should be the real effect of those price changes from a payer’s perspective (in our case Medicaid; individual results will vary).

The green bubbles on the right of the Bubble Chart viz (screenshot below in Figure 2) are the generic drugs that experienced a price decline (i.e. got cheaper) in the latest survey, while the yellow/orange/red bubbles on the left are those drugs that experienced a price increase. The size of each bubble represents the dollar impact of the drug on state Medicaid programs, based on utilization of the drugs in the most recent trailing 12-month period (i.e. bigger bubbles represent more spending). Stated differently, we simply multiply the latest survey price changes by aggregate drug utilization in Medicaid over the past full year, add up all the bubbles, and get the total inflation/deflation impact of the survey changes.

Figure 2

Source: Data.Medicaid.gov, 46brooklyn Research

Overall, in October, there was just over $109 million worth of inflationary drugs, nearly perfectly offset just under $109 million of deflationary generic drugs, netting out to less than $1 million inflation for Medicaid, the closest we have seen to no change since we started this report three years ago.

6. Year-over-year generic oral solid deflation compresses slightly to ~14%

Ever since June 2020, we have been tracking year-over-year generic deflation for all generic drugs that have a NADAC price. We once again weight all price changes using Medicaid’s drug utilization data. This month, deflation on oral solid generics and all generics declined to 14.0% and 11.0%, respectively (Figure 3). If you are a purchaser of generic drugs, a decline in this metric is not ideal as it means costs are declining at a less rapid pace.

Figure 3

Source: Data.Medicaid.gov, 46brooklyn Research

7. Top/notable generic drug decreases this month

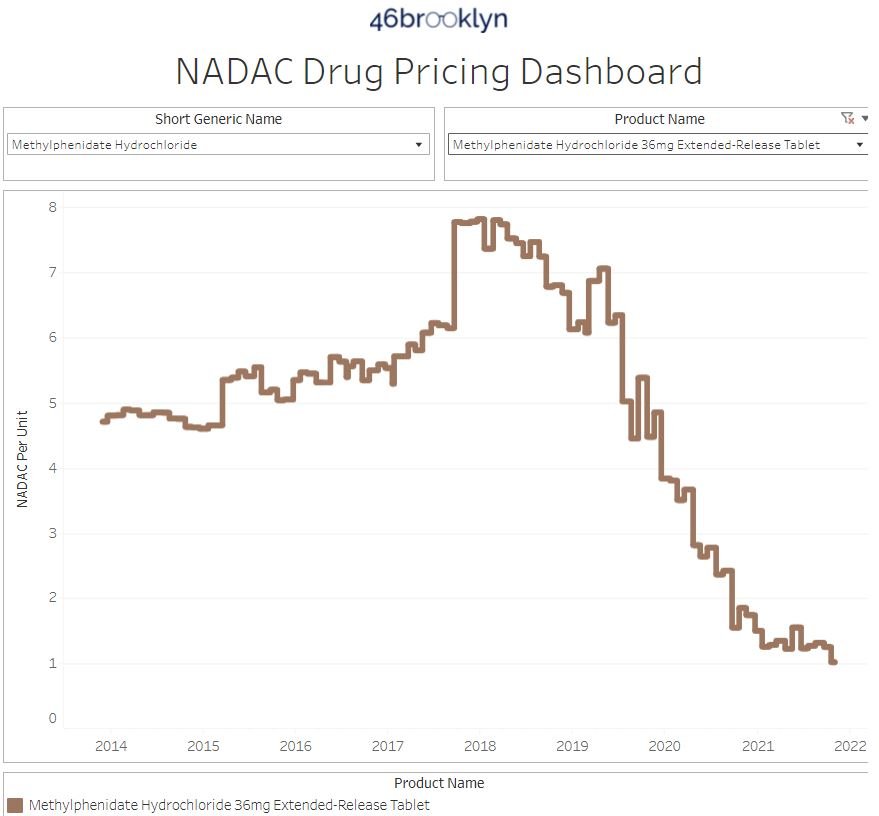

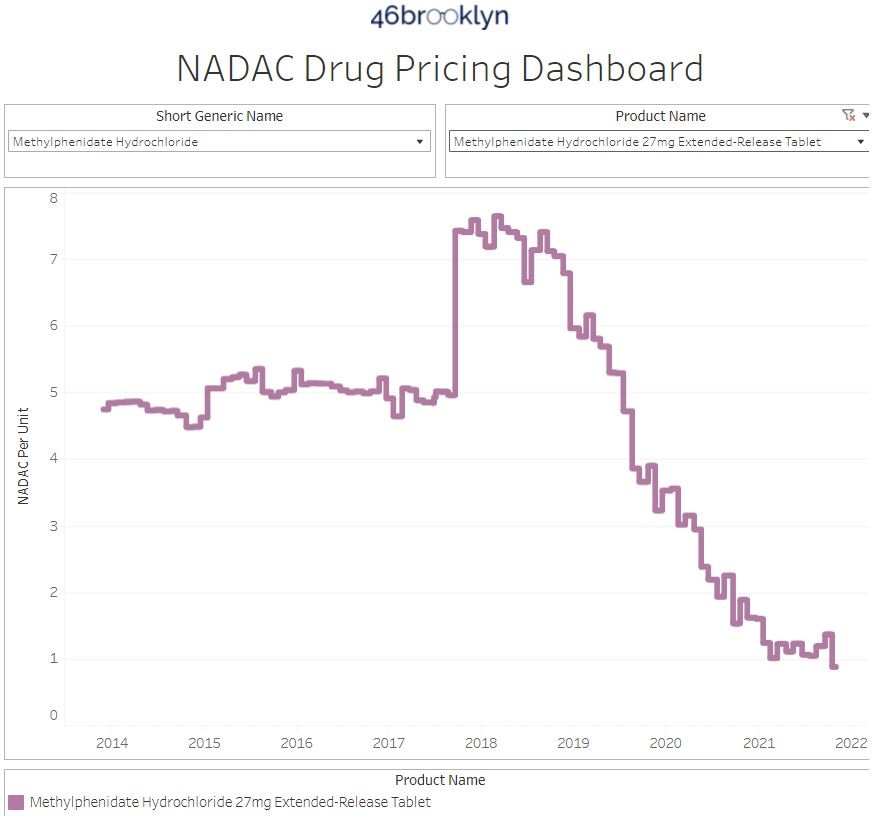

There are several generic drug price decreases this month. The biggest are the ones we’ve probably written the most about in these section and those of course would be our methylphenidate ER products. Generic Concerta 27 mg and 36 mg each fell by double digits this month in NADAC contributing over $10 million in generic deflation (over 10% of the total for this month was on these two drugs). Though we’ve written about them countless times before, their trend charts are below.

8. Top/notable generic drug increases

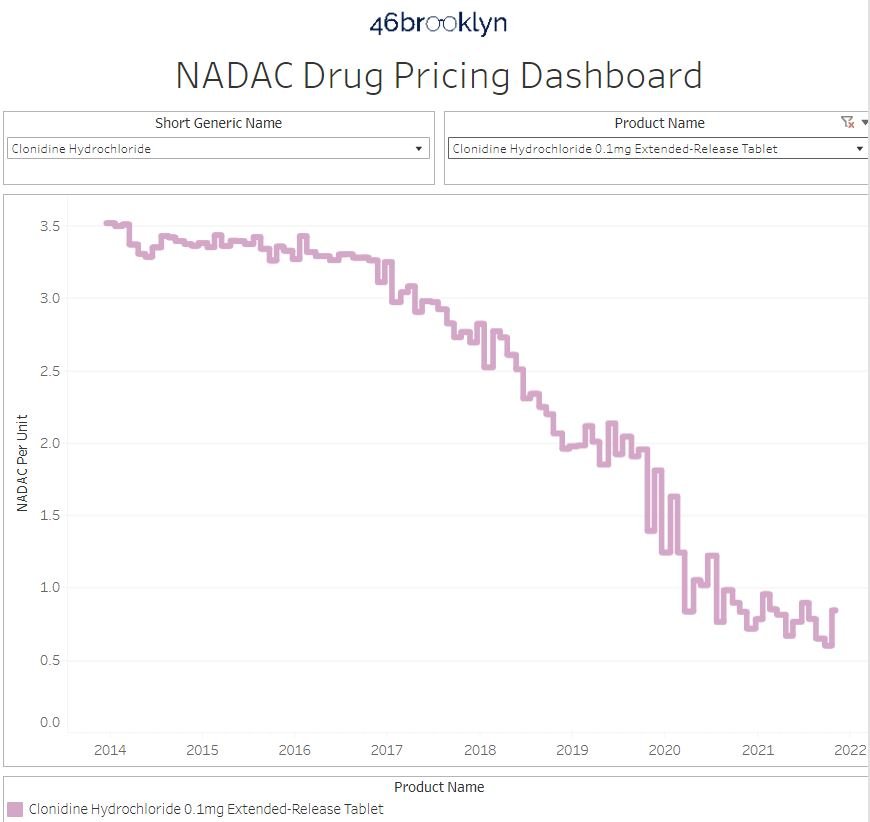

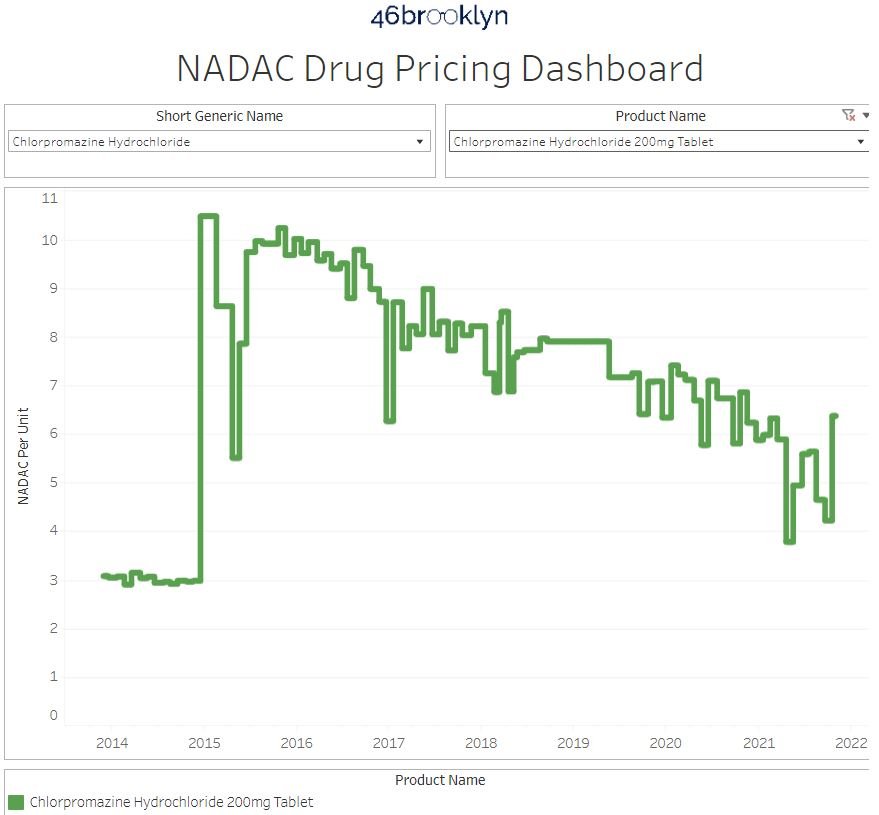

On the increase side of things, the most impactful increases were chlorpromazine 200 mg tablets (51% increase) and clonidine ER 0.1 mg tablet (40.5% increase). Combined, these two products account for $7.3 million in inflationary pressure to Medicaid (or nearly cancelling out the methylphenidate deflation).

In researching these price increase behaviors, we found two studies of note regarding chlorpromazine in 2021. The first is a study in pediatrics to help control agitation and the second was an observational study regarding chlorpromazine and COVID-19 where it was not associated with decreases in patient mortality. We found something similar for clonidine and COVID-19 (apparently everything has been suggested at this point as a potential COVID-19 therapy). Neither of these would suggest an increase in demand based upon new literature.

Nonetheless, the NADAC pricing behavior of these drugs is shown in the gallery below:

That’s all for this month. We hope you all had a happy and healthy Thanksgiving.

This month, 46brooklyn took a trip to Washington DC to talk prescription drug pricing and pharmacy benefits management. First, our CEO Antonio Ciaccia was invited to participate in a special panel discussion for the United States House Committee on Oversight and Reform Republican forum entitled “Reviewing the Role of Pharmacy Benefit Managers in Pharmaceutical Markets.” The forum, hosted by Representative James Comer (R-KY), dove into the highly influential role that pharmacy benefit managers (PBMs) have on the prescription drug supply chain. To view the hearing in its entirety, see below or click here, and to view Ciaccia’s submitted remarks, click here. Thanks to Darrel Rowland, the drug pricing guru at the Columbus Dispatch, who did a great report on the hearing’s play-by-play.

Shortly after the forum, Ciaccia was invited to speak at The Hill’s Future of Healthcare Summit: Tackling Costs & Pathways to Care. The summit focused on addressing the social, economic, and environmental factors that influence health and overall access, and re-examining our traditional models of care to better fit the needs of patients, all while keeping costs in check. To view the second half of the program, where Ciaccia’s segment took place, see below or click here.

Big shout-out to Shelby Livingston at Business Insider for her excellent deep-dive into the world of rebate aggregators, the group purchasing organizations propped up by large PBMs to extract bigger price concessions from drug manufacturers.

Also, great to chat with Michelle Sherman at the Conscious Pharmacist podcast about the impact PBMs have on pharmacists, patients, and plan sponsors.

Lastly, thanks to Jake Zuckerman at the Ohio Capital Journal for chatting with Ciaccia on ivermectin hype in Ohio.